त्वरित लिंक

Shell's $1.7B Na Kika Divestment: What Leveraged Energy Traders Need to Know

डेटा स्नैपशॉट

मुख्य निष्कर्ष

- •Leveraged TALO CFD traders face binary deal-break risk: BP's 30-day preferential right could void the acquisition entirely — a hard stop-loss trigger for long positions.

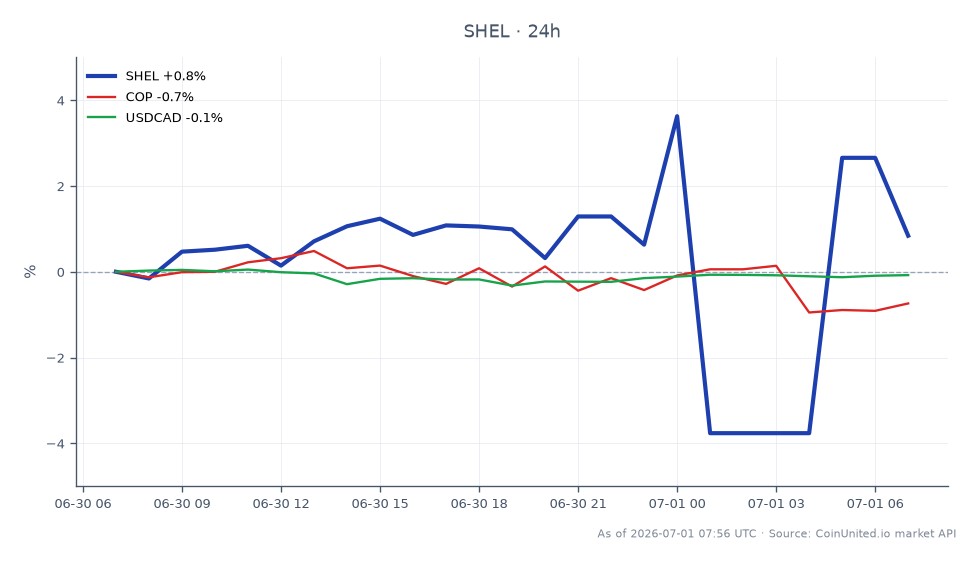

- •SHEL at $77.43 (live) sees incremental upside from $1.7B cash inflow and decommissioning liability transfer, but price reaction is gradual — high-leverage SHEL positions face outsized drawdown risk given the 7.7% intraday range.

- •BP carries short-term event optionality: exercising the preferential right adds capex/decommissioning obligations, potentially pressuring BP equity — a tactical short setup to monitor.

- •Brent and WTI are unaffected — 16,000 boe/d is immaterial to global supply; this is a corporate, not commodity, event.

- •This deal confirms the ongoing pattern of major integrateds divesting mature assets while mid-cap E&Ps scale via acquisition — supportive of the broader energy M&A re-rating thesis.

Shell plc (NYSE: SHEL) has agreed to sell its 50% non-operated working interest in the Na Kika platform and associated Gulf of America fields, plus its 100% owned Coulomb subsea tieback, for $1.7 bill

Event Summary

Shell plc (NYSE: SHEL) has agreed to sell its 50% non-operated working interest in the Na Kika platform and associated Gulf of America fields, plus its 100% owned Coulomb subsea tieback, for $1.7 billion in total consideration. According to PR Newswire and World Oil, the buyers are subsidiaries of Talos Energy Inc. (TALO) and Ridgewood Energy, with an effective date of July 1, 2025 and expected closing by end-2026. Talos disclosed its share at $850 million, with net cash consideration of $450–500 million after interim cash flow adjustments. Shell retains royalty, offtake rights, and contingent upside payments through 2027 — shifting from operational exposure to a capital-lighter model.

A critical near-term variable: BP plc holds a 30-day preferential purchase right to acquire Shell's interest on identical terms, making BP's decision a short-term binary event risk for both TALO and BP equity.

Leverage Impact Analysis

This is a stock-specific catalyst with asymmetric leverage implications across three names.

SHEL CFDs are the most liquid trade here. At CoinUnited.io's up to 2000x leverage on stock CFDs, position sizing discipline is critical. With SHEL currently trading at $77.43 (24h range: $73.90–$79.57, per live data), the divestment is incrementally positive — $1.7B cash inflow plus decommissioning liability removal supports buyback/dividend capacity. However, the price reaction is likely muted and gradual, not a gap event.

Example: A 50x long SHEL CFD opened at $77.43 controls $3,871.50 per unit. A 1% adverse move to $76.66 generates a ~50% drawdown on margin — illustrating how even modest post-announcement drift can be punishing at high leverage. With 24h volatility already spanning $5.67 (7.7% range), sizing conservatively is warranted.

TALO equity is the higher-conviction leverage play. Adding ~16,000 boe/d (77% oil) and 23 million boe proved reserves is a portfolio-defining event for a mid-cap E&P. Analyst estimate revisions and re-rating potential are material. However, BP's preferential right introduces binary deal-break risk — leveraged TALO longs should monitor BP's 30-day window closely, as an exercise decision reshuffles the entire trade thesis.

BP CFDs carry event optionality: if BP exercises its preferential right, BP equity faces incremental capex and decommissioning obligations, which could pressure short-term price action — a potential short setup for traders tracking the decision timeline.

Cross-Market Impact

The deal has minimal commodity market impact. The Na Kika fields produced ~16,000 boe/d in Q1 2026 — negligible versus global supply — so Brent crude oil and WTI benchmarks are unaffected. This is a corporate ownership transfer, not a supply event.

For sector context, this deal reinforces the ongoing energy, pharma & tech acquisition wave — large integrated majors high-grading portfolios while mid-cap E&Ps scale via acquisition. Peers like Chevron Corporation and ConocoPhillips may see marginal read-through as investors benchmark Gulf of America deepwater valuations. The global acquisition & consolidation wave theme supports a broader re-rating of mid-cap offshore E&Ps.

FX impact is negligible. The transaction is USD-denominated with no material effect on USD/CAD or USD/NOK — both oil-correlated pairs that would only move on supply-side surprises, not ownership transfers.

For broader 2026 stocks market outlook context, this is part of a pattern of capital discipline among majors — proceeds likely recycled into buybacks rather than reinvestment, which is net positive for SHEL's total return profile.

Trading Considerations

The key binary event is BP's 30-day preferential right decision. If BP exercises, TALO's acquisition thesis collapses entirely — a clean stop-loss trigger for leveraged TALO longs. If BP passes, the deal proceeds and TALO re-rates on the production/reserves addition. Watch for any BP management commentary in the near term as the primary catalyst.

For SHEL, the $73.90 24h low represents near-term support, with $79.57 as resistance. Given the incremental-positive nature of the divestment, the trade is a hold/accumulate rather than a momentum entry. Monitor Shell management commentary on capital deployment of the $1.7B proceeds for the next meaningful catalyst.

Trade Shell PLC on CoinUnited.io

Trade SHEL with up to 800xx leverage → | Create Free Account

अक्सर पूछे जाने वाले प्रश्न

BP has a 30-day window to acquire Shell's interest on identical terms — if exercised, the Talos deal is void and TALO loses its primary catalyst, likely triggering a sharp reversal. Leveraged TALO longs should treat BP's decision as a hard binary risk event and size positions accordingly.

जारी रखें अन्वेषण

अस्वीकरण: यह संक्षेप केवल शैक्षिक उद्देश्यों के लिए है और यह निवेश सलाह नहीं है।