त्वरित लिंक

Magnolia Oil & Gas Emerges as Front-Runner in $4B+ WildFire Energy Buyout

डेटा स्नैपशॉट

मुख्य निष्कर्ष

- •Reuters reports WildFire Energy owners Warburg Pincus and Kayne Anderson are exploring a $4B+ sale — no deal confirmed yet.

- •Bloomberg names Magnolia Oil & Gas as the front-runner, making this a potentially transformative acquisition for a mid-cap E&P.

- •A $4B+ valuation for a PE-backed shale asset signals elevated upstream M&A multiples and a still-active private equity exit environment.

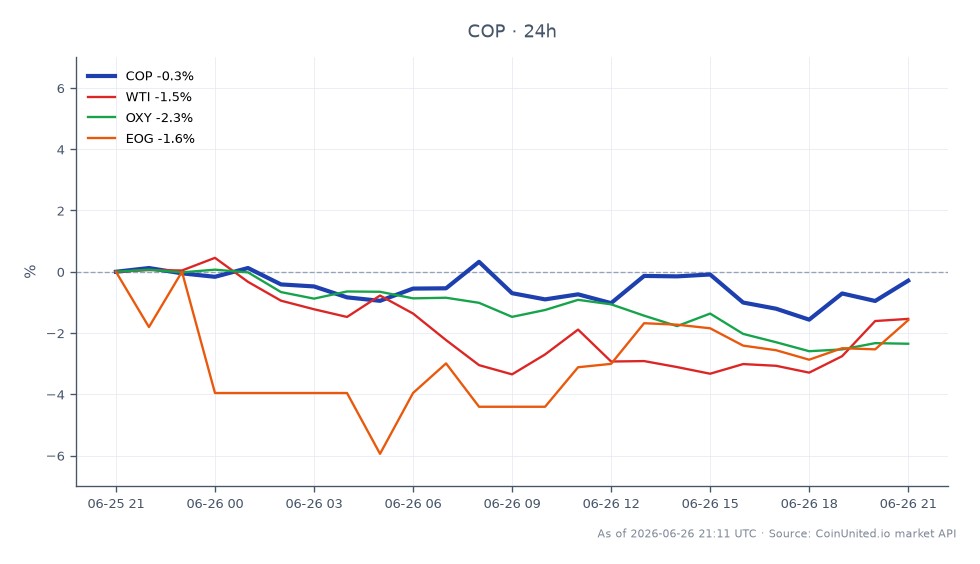

- •Comparable E&P peers (ConocoPhillips, EOG, Occidental) may see modest re-ratings as deal benchmarks for shale acreage are reset upward.

- •Near-term crude oil supply impact is negligible, but sustained shale consolidation is structurally mild-bullish for WTI over a multi-quarter horizon.

According to Reuters, the owners of WildFire Energy — private equity firms Warburg Pincus and Kayne Anderson — are exploring a sale of the U.S. shale operator, with any transaction expected to value t

Event Analysis

According to Reuters, the owners of WildFire Energy — private equity firms Warburg Pincus and Kayne Anderson — are exploring a sale of the U.S. shale operator, with any transaction expected to value the company at $4 billion-plus. Bloomberg has separately named Magnolia Oil & Gas as the front-runner among potential acquirers. This remains an unconfirmed, exploratory process; no deal has been signed.

The significance here extends beyond the two parties directly involved. A $4B+ price tag for a private-equity-backed shale asset signals that upstream M&A multiples remain elevated despite oil price volatility in 2025. Warburg Pincus and Kayne Anderson are sophisticated sellers who would not be running a formal process unless they believed the bid environment was favorable — that itself is a read-through for the broader energy, pharma & tech acquisition wave currently reshaping the sector.

What makes this deal structurally notable is the buyer profile. Magnolia Oil & Gas is a mid-cap E&P — not a supermajor — meaning a $4B+ acquisition would represent a transformative balance-sheet event, not a bolt-on. Investors will immediately focus on how Magnolia would finance the deal (equity issuance, debt, or a combination), which assets WildFire brings to the table in terms of acreage and production, and whether the acquisition changes Magnolia's capital return profile. This is precisely the dynamic explored in the global acquisition & consolidation wave reshaping mid-cap energy.

The broader backdrop is a shale sector where private-equity exit windows have become narrower. Large-cap consolidation (ConocoPhillips, Occidental, EOG Resources have all been active in M&A conversations) has compressed the field of credible strategic buyers. A mid-cap like Magnolia stepping up for a $4B asset suggests the consolidation wave is now filtering down-market, with implications for how PE-backed shale inventory gets valued and absorbed going forward.

What This Means for Traders

The most direct equity impact falls on Magnolia Oil & Gas (MGY), which could see pressure if markets price in acquisition risk — dilution, leverage increase, or integration uncertainty — alongside any upward re-rating if the deal is seen as accretive. Comparable public E&P names including ConocoPhillips, EOG Resources, and Occidental Petroleum may see modest sympathy moves as the transaction reinforces deal-multiple benchmarks for shale assets. Traders focused on the M&A acquisition wave should treat this as a sector sentiment signal rather than a direct catalyst for large-caps.

On the commodities side, the deal does not alter near-term WTI Light Crude Oil supply in any material way. However, sustained consolidation in U.S. shale — where acquirers typically rationalize capex and prioritize returns over production growth — is structurally mildly bullish for crude over a multi-quarter horizon. Volatility on individual E&P names is the more immediate trade, while crude itself remains macro-driven. The cross-sector acquisition repricing theme favors watching mid-cap E&P names for M&A premium pricing as the deal process matures.

This news broke during active market hours, so positioning in related equity CFDs on CoinUnited can be adjusted in real time. Monitor for deal confirmation or denial — either outcome will drive a sharper directional move than the current rumor-stage positioning.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

अक्सर पूछे जाने वाले प्रश्न

According to Reuters, the owners are exploring a sale — this is a preliminary process, not a signed deal. Outcome risk (confirmation, repricing, or abandonment) remains high.

जारी रखें अन्वेषण

अस्वीकरण: यह संक्षेप केवल शैक्षिक उद्देश्यों के लिए है और यह निवेश सलाह नहीं है।