त्वरित लिंक

Bessent's Greenspan 'Tap the Brakes' Signal: Leverage Playbook for USD/JPY, EUR/USD & Cross-Asset Repricing

डेटा स्नैपशॉट

मुख्य निष्कर्ष

- •Treasury Secretary Bessent invoked the Greenspan 1997 'tap the brakes' template unprompted — Renaissance Macro's Neil Dutta reads this as a green light for a September Fed hike by Chair Warsh.

- •A September hike would invert prior market pricing (cuts expected), creating mispricing opportunities in STIRs, USD crosses, and rate-sensitive assets.

- •Leverage impact: 100x long USD/JPY CFDs at 161.67 amplify every pip ~$620 — extended BoJ-Fed divergence supports the trade, but intervention risk above 162 is elevated.

- •Cross-market: Front-end yields (2y) rise, DXY strengthens, gold faces real-yield headwinds, and NASDAQ duration names are most exposed to valuation compression.

- •Crypto is incrementally bearish on the margin — BTC and ETH trade as high-beta liquidity proxies and are negatively exposed to tighter marginal financial conditions.

According to InvestingLive, U.S. Treasury Secretary Scott Bessent made an unprompted reference to Alan Greenspan's 1997 'tap the brakes' rate hike in a speech to business leaders in New York — a singl

Event Summary

According to InvestingLive, U.S. Treasury Secretary Scott Bessent made an unprompted reference to Alan Greenspan's 1997 'tap the brakes' rate hike in a speech to business leaders in New York — a single pre-emptive increase that did not derail expansion and was followed by three cuts. Renaissance Macro's Neil Dutta interpreted this as Bessent giving Fed Chair Kevin Warsh a deliberate 'green light' to hike rates in September 2026.

The signal carries weight because Bessent raised the analogy without prompting, and the template aligns precisely with the Fed's dot plot, which shows a median projection of one hike in 2026 followed by one cut in 2027. As InvestingLive notes, a September hike would represent "a complete inversion of the rate path markets had priced coming into 2026," which had been skewed toward cuts — making this the defining Fed macro policy crossroads event of the summer.

Leverage Impact Analysis

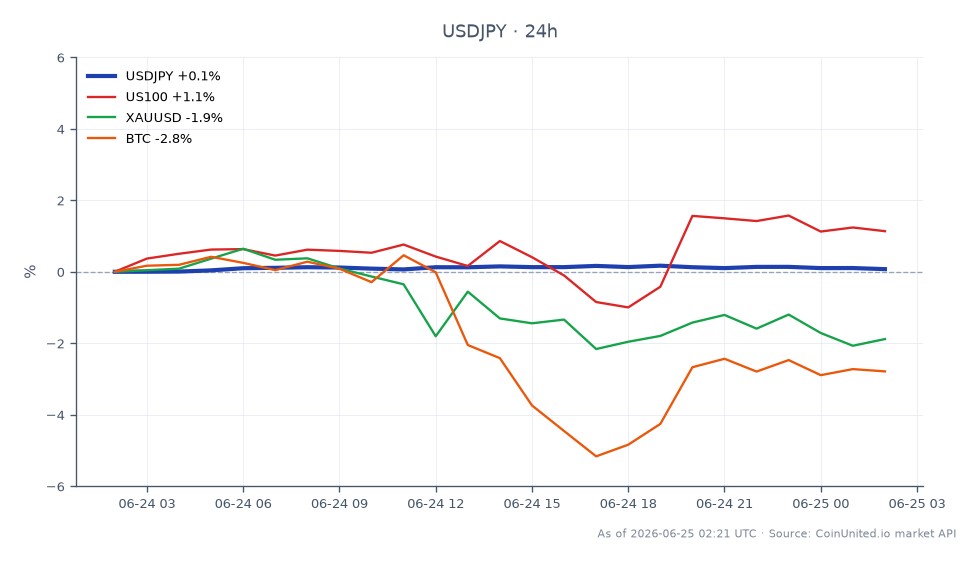

USD/JPY is the highest-conviction leverage trade. USD/JPY is currently trading at $161.67 (24h range: $161.56–$161.79), already elevated near multi-year highs. A September hike repricing widens the BoJ-Fed rate differential further, structurally supporting yen shorts.

- -A 100x long USD/JPY CFD entered at 161.67 would see ~$620 P&L per pip move. A 50-pip extension toward 163 generates ~$31,000 gain on a $1,000 margin — but also faces ~$620 loss per pip on any BoJ intervention flush. See our USD/JPY & BoJ divergence guide for full intervention risk mapping.

- -Short EUR/USD is the mirror trade. The euro/US dollar pair faces headwinds as rate differentials reprice against ECB hold/cut mode. A 200x short EUR/USD position at current levels amplifies every 10-pip move to ~2x notional — position sizing must account for the asymmetric risk of a Bessent walk-back.

- -Liquidation risk: Leveraged long risk-asset positions (crypto, Nasdaq CFDs) opened in the prior cut-pricing regime face the greatest unwind pressure. Traders running >50x long US100 CFDs should monitor real-rate moves closely — even a 20bp front-end yield shift can compress Nasdaq valuations and trigger cascading stops.

Cross-Market Impact

Rates & FX (primary channel): Front-end U.S. Treasury yields (2y) are most exposed — a September hike repricing pushes 2y yields higher, flattening or bear-flattening the curve. DXY strength flows through to all USD crosses, with JPY, CHF, and EUR most vulnerable given their central banks' dovish-to-neutral stances.

Equities: The S&P 500 and NASDAQ-100 face dual pressure from higher real yields compressing duration-sensitive valuations. However, the "one hike then cuts" soft-landing framing limits full risk-off. Bond-proxy sectors (REITs, Utilities) are the clearest underperformers; Financials may outperform on net interest margin expansion. Detailed index cycle analysis is available in our S&P 500 FOMC cycle guide.

Gold: Higher real yields and a stronger USD are structurally negative for gold. The gold vs. USD inverse relationship is the key framework here — if the market prices the Greenspan template as inflation-insurance (not overtightening), gold may find support on the medium-term soft-landing narrative, but near-term pressure is the base case.

Crypto: Bitcoin and ETH trade as high-beta liquidity assets. A shift from cut-pricing to hike-pricing tightens marginal liquidity conditions — incrementally bearish for BTC perpetual longs. Monitor crypto funding rates on CoinUnited.io for confirmation of positioning stress.

Trading Considerations

The key asymmetry: Bessent's remark is analyst-interpreted signaling, not a formal Fed decision. If September hike odds fail to reprice significantly in OIS markets, or if Warsh pushes back, USD longs and rate-sensitive shorts face sharp reversals. The Fed & ECB rate patience macro repricing theme suggests volatility remains elevated through Q3.

Watch USD/JPY above 162.00 for BoJ intervention risk (levels flagged in prior CoinUnited pulses); EUR/USD support around recent lows; and VIX for any spike signaling risk-off rotation that could override the rate-hike narrative.

Trade US Dollar / Japanese Yen on CoinUnited.io

Trade USDJPY with up to 2000xx leverage → | Create Free Account

अक्सर पूछे जाने वाले प्रश्न

USD/JPY at 161.67 already reflects elevated rate-differential expectations — a further repricing toward a September hike widens the BoJ-Fed spread and supports extended yen weakness. At 100x leverage, each pip is worth ~$620, so a 50-pip move to 162.17 yields ~$31,000 on $1,000 margin, but BoJ intervention above 162 can reverse that in minutes.

जारी रखें अन्वेषण

अस्वीकरण: यह संक्षेप केवल शैक्षिक उद्देश्यों के लिए है और यह निवेश सलाह नहीं है।