Quick Links

China's Indium Phosphide Export Controls Threaten AI Data Centre Rollout — Semiconductor Supply Chain Repricing Ahead

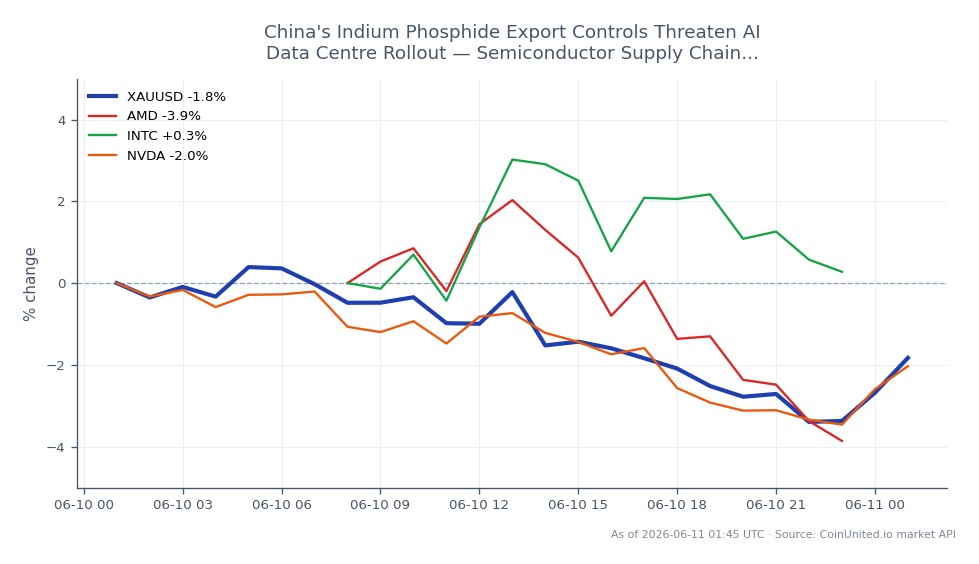

Data Snapshot

Key Takeaways

- •China has extended export controls to indium and InP-related inputs, targeting the upstream substrate supply chain for AI optical transceivers (800G–1.6T).

- •InP wafers are identified as the #1 AI hardware bottleneck for 2026; supply-demand rebalancing is not expected before 2026 per IntelliEPI's chairman.

- •Leverage risk: A 50x long Gold CFD at $4,110.44 faces liquidation near $4,028 — within $4 of today's 24h low of $4,023.98; position sizing is critical.

- •Cross-market: Non-Chinese InP suppliers (JX Metals) and Taiwanese III-V foundries are structural beneficiaries; China-dependent optical-component makers face margin and volume risk.

- •NVDA and AMD CFD longs are indirectly exposed — InP shortages don't hit GPU production directly but can cap AI data-centre deployment velocity, compressing the demand growth narrative.

China has extended its critical materials export control regime to indium and indium phosphide (InP)-related products, according to industry research and supply-chain analysis. The move follows earlie

Event Summary

China has extended its critical materials export control regime to indium and indium phosphide (InP)-related products, according to industry research and supply-chain analysis. The move follows earlier restrictions on gallium and germanium and targets upstream inputs essential for InP substrates — the compound semiconductor wafers underpinning high-speed optical transceivers (800G–1.6T) in AI data centres. InP-based components power electro-absorption modulated lasers (EMLs) and photodiodes that handle the data transmission layer inside hyperscale AI infrastructure. Industry commentary frames InP wafers as the #1 hardware bottleneck risk for 2026 AI deployment, ahead of GPUs.

Demand context is stark: JX Metals projects InP wafer surface area growth of approximately 30% in FY 2025, driven entirely by AI infrastructure demand. IntelliEPI's chairman has stated publicly that capacity increases of 20–30% by substrate suppliers are not keeping pace with demand, and that supply-demand balance may not be restored before 2026. China's export-control escalation — covering permitting regimes for indium-related inputs — introduces additional friction into an already structurally tight market, consistent with the broader semiconductor supply chain geopolitics theme reshaping critical tech supply.

Leverage Impact Analysis

Gold (XAUUSD) is trading at $4,110.44 (24h range: $4,023.98–$4,118.27, +1.21%), receiving incremental safe-haven and geopolitical-risk-premium support from this event. The InP export controls reinforce the broader semiconductor geopolitical supply chain repricing narrative — a regime that historically correlates with gold inflows as investors hedge tech-supply-chain inflation and US–China decoupling risk.

Leverage scenario — Gold CFD (XAUUSD):

- -A 50x long Gold CFD entered at $4,110.44 carries a liquidation threshold approximately 2% below entry (~$4,028), dangerously close to today's 24h low of $4,023.98. Position sizing must account for this proximity.

- -A 20x long offers more buffer, with liquidation near $3,904 — outside today's range but still exposed to any reversal driven by hawkish Fed repricing (see recent CPI-driven gold selloffs).

- -The cross-asset tension is critical: gold is simultaneously supported by geopolitical risk (InP/China controls) and pressured by Fed hawkishness. High-leverage longs face binary risk from macro data prints.

For NVIDIA Corporation and Advanced Micro Devices, Inc. CFDs: the InP bottleneck does not directly constrain GPU production, but it caps the deployable AI compute capacity that drives their demand narrative. A 50x long NVDA CFD faces amplified downside if AI data-centre rollout timelines slip due to optical interconnect shortages — monitor guidance language closely.

Cross-Market Impact

Equities: AI infrastructure names bifurcate on this news. Non-Chinese InP suppliers (JX Metals, IntelliEPI) and Taiwanese III-V foundries (LandMark, WIN Semiconductors) stand to command pricing power in a constrained market. Conversely, firms with China-centric upstream exposure face permitting delays and volume risk. The NASDAQ 100 Index has indirect exposure via optical-communications and AI-infrastructure weighting — any rollout delay narrative pressures the index's AI-capex growth premium. This feeds directly into the AI infrastructure capital reallocation dynamic already repricing sector multiples.

Commodities: Gold's geopolitical risk premium receives marginal support. Palladium and platinum — also used in advanced electronics manufacturing — may see sympathy bids if the critical-materials-weaponization theme broadens. Indium itself is a thinly traded industrial metal; tighter Chinese export controls historically drive stockpiling among non-Chinese buyers, supporting spot prices.

Forex: Japan (JX Metals) and Taiwan (III-V foundries) are positioned as beneficiaries of supply-chain rerouting. Incremental high-value export strength is modestly supportive of JPY and TWD at the margin, though this is a second-order effect.

Trading Considerations

Gold's key levels: resistance at the 24h high of $4,118.27; support at $4,023.98 (24h low). A sustained break below $4,024 would invalidate the current geopolitical risk-premium bid and expose leveraged longs to rapid drawdown. The gold vs. US dollar inverse relationship remains the primary driver — Fed macro signals dominate over geopolitical catalysts in the near term.

For semiconductor-linked equities, watch AXT (AXTI) earnings commentary on Chinese permitting timelines and Lumentum/Coherent sourcing disclosures as leading indicators of InP supply stress propagating into optical module margins.

Trade Gold / US Dollar on CoinUnited.io

Trade XAUUSD with up to 2000xx leverage → | Create Free Account

Frequently Asked Questions

Gold at $4,110.44 receives marginal geopolitical risk-premium support, but 50x longs face liquidation near $4,028 — just $4 above today's 24h low of $4,023.98. Reduce leverage or widen stops before any macro catalyst (e.g., Fed speakers) that could override the geopolitical bid.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.