Quick Links

Alcoa Drops 9% on $60M Q2 Alumina Hit — Leverage Scenarios & Cross-Market Ripples

Data Snapshot

Key Takeaways

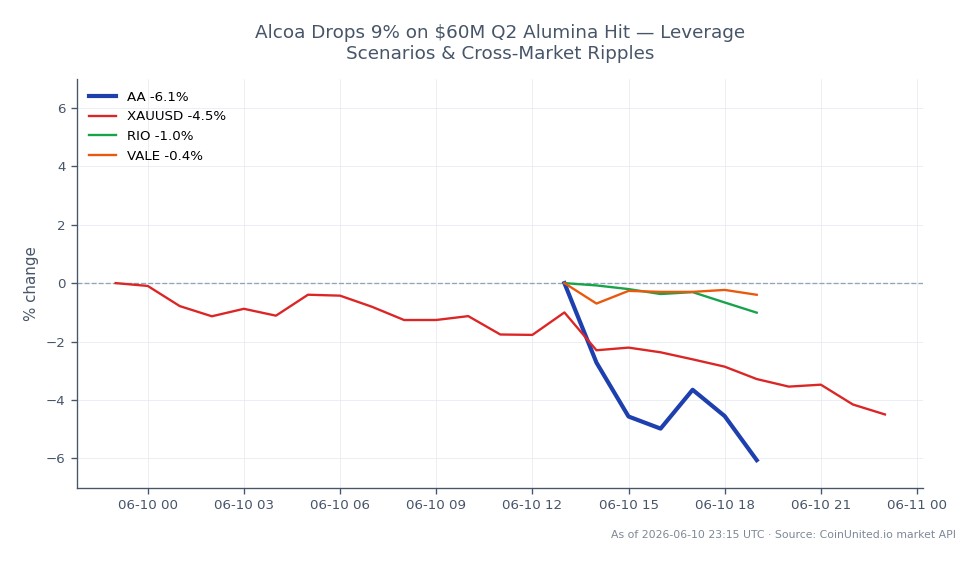

- •AA fell 9.36% to $65.72, with the $60M Q2 hit exceeding Alcoa's own prior internal estimates by $45M+ — making this an incremental, not pre-priced, guidance shock.

- •Leveraged long AA CFD traders entering above $70 pre-disclosure face margin wipe scenarios at 20x–50x; fresh short entries at $65.72 risk mean-reversion if Pinjarra disruption is ruled weather-driven.

- •The ~$20M energy cost component linked to Middle East conflict reinforces the macro inflation pressure narrative, providing indirect support for gold as an inflation hedge.

- •Rio Tinto and Vale face sentiment read-through risk given shared exposure to energy-intensive refining operations and Australian resource production.

- •The key trading decision point is distinguishing transitory (Pinjarra weather) vs. structural (energy costs) drivers — analyst revisions in the next 48 hours will be the primary re-rating signal.

Alcoa Corporation (AA) disclosed in an investor presentation that it expects approximately $60 million in negative impact to its Alumina segment in Q2, split between ~$30 million in higher production

Event Summary

Alcoa Corporation (AA) disclosed in an investor presentation that it expects approximately $60 million in negative impact to its Alumina segment in Q2, split between ~$30 million in higher production costs at the Pinjarra refinery in Western Australia (disrupted by Cyclone Narelle) and ~$20 million in elevated energy input costs tied to Middle East conflict. The company simultaneously cut its Q2 third-party alumina shipment guidance by 120,000 metric tons. According to market data, AA fell 9.36% on the day, touching an intraday low of $65.66 against a prior high of $71.56 — confirming the market treated this as material, incremental guidance deterioration, not a pre-priced risk.

This is a current-quarter earnings revision with dual drivers: operational (weather/cyclone) and structural (energy inflation). The magnitude exceeded Alcoa's own internal estimates by more than $45 million, underscoring that this caught even management off-guard.

Leverage Impact Analysis

With AA currently trading at $65.72 after a ~$6.80 intraday decline, leveraged traders face asymmetric risk on both sides.

Long squeeze scenario: A trader holding a 50x long AA CFD entered at $71.00 (pre-disclosure) now sits on a ~9.6% adverse move. At 50x leverage, that translates to a ~480% loss on margin — a position well past standard liquidation thresholds. Even a 20x long from $68.00 would represent a ~100% margin wipe.

Short entry context: Traders initiating fresh 20x short CFD positions at current levels ($65.72) face a key risk: if the market reprices the Pinjarra disruption as a *one-time weather event*, a mean-reversion rally toward $70–71 would generate a ~8% adverse move, liquidating positions with less than ~12.5% margin buffer at 20x.

This type of earnings miss revenue shock typically produces a post-gap drift pattern — initial flush followed by either continuation (if structural) or recovery (if weather-driven). Position sizing should reflect that distinction. Monitor funding rates and open interest on CoinUnited.io for directional conviction signals before adding leverage.

Cross-Market Impact

Mining peers: Rio Tinto plc and Vale S.A. share exposure to energy-intensive refining and Australian operational risk. If energy cost pressures are systemic rather than Alcoa-specific, peer margins face similar read-through — particularly for alumina and bauxite-linked operations.

Commodities: Reduced Q2 alumina shipments (–120k tons) tighten near-term supply at the margin. This could modestly support alumina spot prices, which feeds upstream into aluminum cost floors. Gold benefits indirectly as the energy-inflation narrative reinforces the inflation hedge thesis — Middle East conflict driving industrial input costs higher is a macro confirmation point for safe-haven demand.

Macro/FX: Alcoa explicitly links ~$20M of the hit to energy prices from Middle East tensions, reinforcing that geopolitical risk is still transmitting into heavy industry margins. This is a micro datapoint consistent with macro inflation pressure narratives. AUD exposure is limited at the single-stock level, but traders watching commodity FX should note the operational disruption risk to Australian resource output.

Materials sector: Broader materials indices and metals/mining ETFs may face sentiment drag. Alcoa is a bellwether in the aluminum chain — guidance cuts here can prompt analysts to revisit cost assumptions across energy-intensive producers sector-wide.

Trading Considerations

Key levels: AA's intraday low of $65.66 represents immediate support. Resistance sits near the pre-disclosure range of $70–71.56. The stock has already absorbed the initial shock; the next catalyst is whether Q2 earnings (when reported) confirm the $60M estimate or reveal further deterioration. Watch for analyst estimate revisions in the next 24–48 hours as the primary re-rating trigger.

Risk factors: the energy-cost component (~$20M) is potentially persistent, while the Pinjarra disruption (~$30M) may be weather-related and transitory. How the market splits these two drivers will determine whether AA stabilizes near current levels or faces continued multiple compression. Traders considering earnings miss recovery plays should wait for stabilization confirmation before positioning.

Trade Alcoa Corporation on CoinUnited.io

Frequently Asked Questions

At $65.72, a 10x–15x long CFD limits liquidation exposure to roughly a further 6–10% drawdown — manageable if the Pinjarra disruption is weather-driven and one-off. Anything above 20x requires a confirmed technical base and should await analyst revision clarity in the next 24–48 hours.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.