Quick Links

US Judge Approves Visa & Mastercard's $38B Swipe Fee Settlement: What It Means for Payments and Retail Traders

Data Snapshot

Key Takeaways

- •US judge approved the $38B Visa/Mastercard interchange settlement, ending ~20 years of antitrust litigation with binding fee caps (10bps reduction for 5 years; 1.25% cap for 8 years).

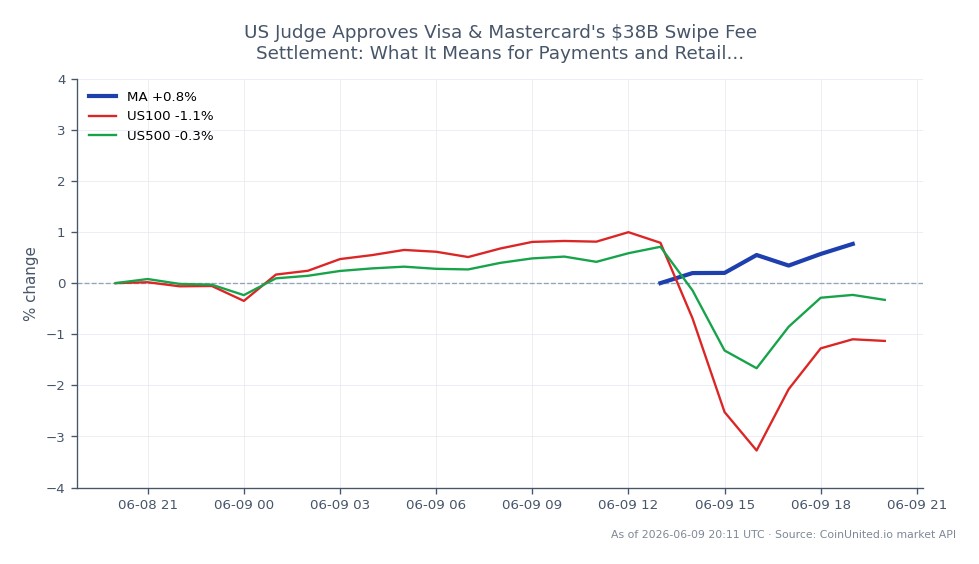

- •Mastercard trading at $494.77 (+2.04%) suggests markets are initially pricing litigation resolution as a positive catalyst, but analyst model revisions for margin compression may weigh in subsequent sessions.

- •Large US merchants (retail, QSR, travel) are the clearest beneficiaries via lower acceptance costs and expanded card-steering rights — watch for positive revisions in consumer discretionary and staples names.

- •Card-issuing banks face secondary pressure as lower interchange compresses card portfolio economics and potentially forces rewards program cuts.

- •The ruling sets a legal precedent that could accelerate interchange reform in other jurisdictions, adding to long-term regulatory risk for global card network take rates.

A US federal judge has approved the landmark $38 billion antitrust settlement between Visa Inc. and Mastercard Inc. and US merchants over credit card interchange (swipe) fees, as reported by The Daily

Event Analysis

A US federal judge has approved the landmark $38 billion antitrust settlement between Visa Inc. and Mastercard Inc. and US merchants over credit card interchange (swipe) fees, as reported by The Daily Record and FStech. The deal supersedes a previously rejected ~$30 billion proposal that a judge dismissed in 2024 as offering "paltry" savings and inadequate merchant flexibility. This revised settlement directly addresses those objections, making court approval a significant legal milestone that ends roughly 20 years of litigation.

The core financial terms are material: Visa and Mastercard must reduce the combined average effective credit interchange rate by 10 basis points for five years, and cap standard consumer credit card interchange at 1.25% for eight years — well below the typical 2.0–2.5% merchants currently absorb. According to settlement filings, merchants also gain expanded surcharging rights (up to 3%, largely unfettered) and the ability to decline higher-cost premium and commercial cards. Nobel laureate economist Joseph Stiglitz estimated total merchant savings could exceed $200 billion over the settlement horizon.

This is a regulatory final ruling market catalyst with a clear structural dimension. Unlike a one-time fine, the fee caps and merchant steering rights create a medium-term structural headwind on card network revenue that will compound through 2031–2033. What separates this outcome from past settlements is the explicit behavioral constraint on pricing power — not just a cash payment — alongside the shift in the "honor all cards" rule that has protected high-fee premium card volume for decades.

Beyond Visa and Mastercard, the ruling reinforces that US courts are prepared to enforce antitrust constraints on card network rules, raising the risk that regulators elsewhere accelerate their own interchange reform agendas — an extension of the global regulatory pressure theme already visible in EU interchange caps and Australia's card surcharging framework.

What This Means for Traders

For equity traders, the near-term read on Visa and Mastercard is a two-sided setup. The headline creates downward pressure through analyst model revisions — lower US credit interchange yield and margin compression over a 5–8 year horizon. Yet the removal of a 20-year litigation overhang is a genuine multiple-expansion catalyst: legal risk has been a persistent discount factor for both names. Mastercard is currently trading at $494.77 (+2.04% on the day per live market data), suggesting the market is initially digesting the litigation-resolved angle as constructive, though sustained upside depends on how sell-side analysts ultimately recalibrate earnings models.

The clearest relative-value trade is card networks versus large-volume merchants. Retailers — particularly big-box, grocery, QSR, and travel — gain direct acceptance cost relief plus the ability to steer customers away from expensive premium cards. For traders tracking the S&P 500 Index or NASDAQ 100 Index, the index-level impact is modest but directionally tilted: Visa and Mastercard face a slight drag while consumer discretionary and staples constituents see incremental cost tailwinds. Card-heavy bank issuers (JPMorgan, Citigroup, Capital One) face a secondary hit, as lower interchange compresses card portfolio economics and may force rewards program devaluations over time. This is worth monitoring in the context of the broader financials and industrials earnings beat cycle.

The settlement also has an indirect narrative tailwind for alternative payment rails. Persistent merchant frustration with card fees — even after this deal, retail trade associations called it "window dressing" — reinforces the long-term case for stablecoin payment infrastructure and account-to-account solutions. That narrative supports names in the fintech ecosystem, though the direct tradeable impact on crypto markets is limited.

Trade Mastercard Incorporated on CoinUnited.io

Frequently Asked Questions

It depends on the time horizon — near-term, the fee caps create measurable revenue headwinds that analysts will need to model; medium-term, removing 20 years of legal risk can support multiple expansion. Watch for sell-side EPS revisions in the days following approval for directional confirmation.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.