Quick Links

Pentagon's WuXi AppTec Military-List Filing: What the Same-Day Withdrawal Means for Leveraged Traders

Key Takeaways

- •The DoD posting and same-day withdrawal is confirmed and documented — it is a real policy signal, not a rumor, but the final regulatory outcome remains unresolved.

- •Leverage risk is elevated: binary regulatory catalysts (re-posting or formal exemption) can gap prices sharply; traders should reduce position sizing to 5x–10x range rather than using maximum leverage on WuXi AppTec CFDs.

- •The withdrawn list also included Alibaba, Baidu, and BYD — signaling a broadening sweep that raises the risk premium for China tech and strategic industrial equities across the board.

- •Non-Chinese CROs (US, EU, India) are structural beneficiaries of the 'China+1' outsourcing diversification trend that events like this accelerate.

- •Cross-market FX and commodity impact is second-order and slow-burn; the primary tradeable impact is confined to Chinese biopharma services equities and related China-exposed indices.

As reported by Pharma Manufacturing and Channel NewsAsia, the US Office of the Secretary of Defense briefly posted an updated Section 1260H list — required under the FY2021 National Defense Authorizat

Event Summary

As reported by Pharma Manufacturing and Channel NewsAsia, the US Office of the Secretary of Defense briefly posted an updated Section 1260H list — required under the FY2021 National Defense Authorization Act — that included WuXi AppTec among Chinese companies deemed to operate on behalf of China's military. The notice characterized WuXi AppTec as "indirectly owned" by SASAC and "indirectly affiliated" with the PLA and SASTIND. Critically, the document was withdrawn the same day without explanation, and WuXi AppTec does not currently appear on the official published DoD list.

The same withdrawn update also briefly listed Alibaba, Baidu, BYD, and RoboSense — signaling this is a thematic, policy-driven sweep rather than an isolated compliance event. Congressional pressure to formally add WuXi AppTec remains active, per prior letters from the House China Select Committee.

Leverage Impact Analysis

The same-day withdrawal creates a binary volatility trap for leveraged traders: the designation was real enough to move prices, but its removal leaves the regulatory outcome unresolved — meaning headline risk remains elevated and positions can be whipsawed in either direction without warning.

For a trader holding a 50x long WuXi AppTec CFD, even a 5% adverse move on re-issuance of the list generates a 250% loss on margin — a near-certain liquidation event. Conversely, a 50x short risks a sharp squeeze if WuXi AppTec secures an official exemption or the list remains withdrawn. This cross-border enforcement repricing dynamic is particularly dangerous at high leverage because the catalyst (a DoD filing) can appear or disappear within hours.

Key risk: gap risk on re-posting. If the DoD re-issues the list during Asian trading hours or a weekend, CoinUnited's 24/7 stock CFD trading allows positioning before traditional Western exchanges open — but that same speed advantage means liquidation can also trigger before most traders react. Position sizing at 5x–10x is more appropriate than maximum leverage for binary regulatory events of this type.

Cross-Market Impact

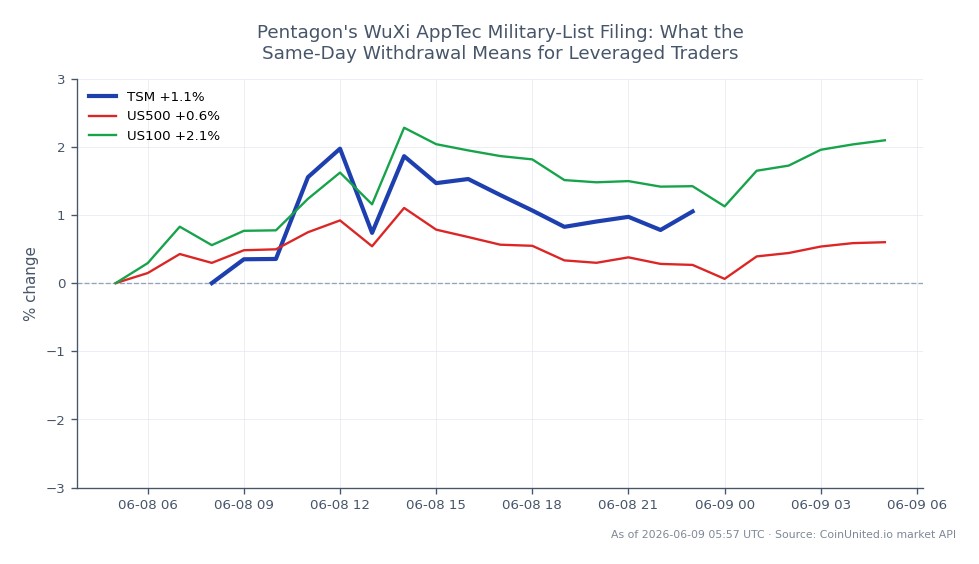

The event's broadest market implication sits within the global regulatory enforcement wave narrative targeting Chinese strategic industries. For the S&P 500 Index and NASDAQ 100 Index, the direct impact is limited — WuXi AppTec is not a benchmark constituent — but the inclusion of Alibaba, Baidu, and BYD in the same withdrawn notice adds regulatory overhang to China-exposed ETFs and EM-heavy allocations.

Taiwan Semiconductor Manufacturing Company Ltd. and other Asia-Pacific tech names face indirect sentiment pressure as investors reassess China-linked supply chain exposure broadly. US and EU large-cap pharma that outsource preclinical work to Chinese CROs face operational risk repricing. Non-Chinese CROs in the US and India are structural beneficiaries of the "China+1" vendor diversification trend accelerated by this event.

FX impact is second-order: incremental US–China tension incrementally supports mild safe-haven flows into USD and JPY, and a weaker CNY bias over the medium term, but this single event is insufficient to move macro FX markets on its own.

Trading Considerations

The key trigger to monitor is re-issuance or finalization of WuXi AppTec's Section 1260H inclusion in a future DoD update, as well as any follow-on actions from Treasury, Commerce, or OFAC. Congressional bills specifically naming the CRO sector would escalate the risk premium materially. Public statements from major US or EU pharma clients about vendor diversification are the most direct earnings-risk signal.

Given the unresolved regulatory status and the pattern of list expansion to biotech/CRO — part of the broader semiconductor supply chain geopolitics playbook applied to life sciences — traders should treat this as a slow-burn structural short thesis on Chinese CROs rather than a single-event momentum trade.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

The withdrawal removes the immediate regulatory catalyst, exposing high-leverage shorts to a potential squeeze if further clarity favors WuXi AppTec; the unresolved status means neither direction is low-risk at maximum leverage.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.