Quick Links

Affirm Locks In $1.7B CPP Deal to Power Up to $8B in Loans — What It Means for AFRM and BNPL Sector

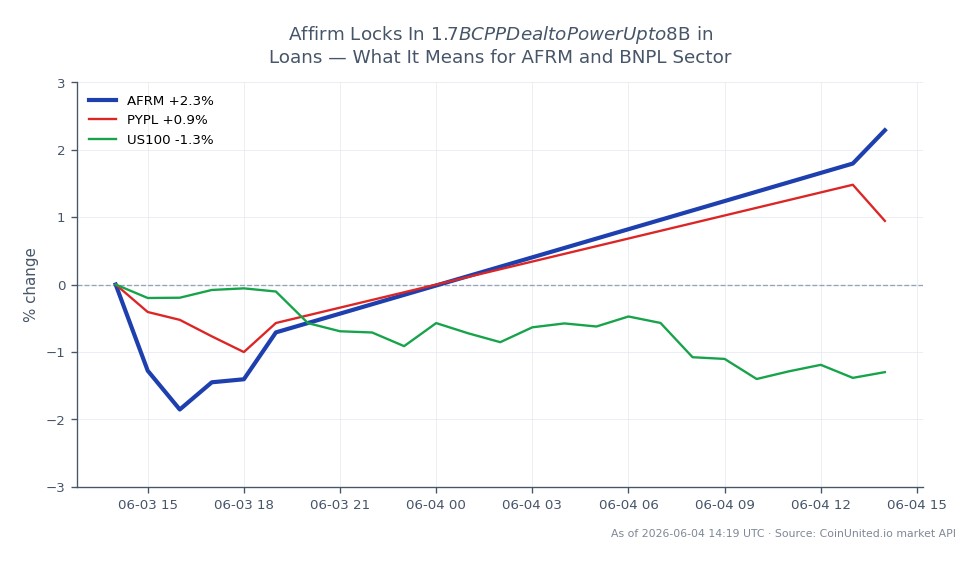

Data Snapshot

Key Takeaways

- •CPP Investments' $1.7B commitment can support up to $8B in loans via revolving BNPL receivables — a ~4.7x implied multiplier that materially expands Affirm's origination capacity.

- •CPPIB's participation is a high-quality institutional validation of Affirm's receivables, reducing funding risk and potentially lowering blended cost of capital.

- •AFRM was up +3.11% to $68.38 at time of writing — momentum supported by this deal following a recent Q3 EPS beat suggests earnings revision risk is skewed upward.

- •Positive sector read-through for BNPL and consumer fintech peers; institutional funding markets remain open for quality receivables despite macro caution.

- •Traders should monitor management guidance on GMV deployment and watch for analyst price-target upgrades as the multi-year funding impact is modeled in.

Affirm Holdings has extended its partnership with CPP Investments (CPPIB) through a $1.7 billion capital commitment designed to support up to $8 billion in consumer installment loans. The implied 4.7x

Event Analysis

Affirm Holdings has extended its partnership with CPP Investments (CPPIB) through a $1.7 billion capital commitment designed to support up to $8 billion in consumer installment loans. The implied 4.7x multiplier reflects the short-duration, revolving nature of buy now, pay later (BNPL) receivables — capital cycles through originations and repayments multiple times per year, effectively amplifying the facility's reach. This is consistent with the mega financing & partnership catalyst playbook that major fintech lenders use to scale without proportionally expanding their own balance sheets.

What distinguishes this deal from routine warehouse facilities is the counterparty. CPP Investments is one of the world's most rigorous institutional allocators, managing over C$600 billion. Its willingness to commit at this scale signals genuine conviction in Affirm's receivables quality and credit performance — a validation that carries far more weight than a bank-arranged warehouse line. This fits squarely within the strategic corporate partnerships theme, where tier-1 institutions anchor the funding stack of high-growth fintech platforms.

For Affirm, the strategic implication is significant. Stable, long-dated institutional funding reduces refinancing risk, potentially lowers blended cost of capital, and removes a key ceiling on gross merchandise volume (GMV) growth. Coming shortly after Affirm's Q3 2026 EPS beat, this deal reinforces a narrative of operational momentum meeting structural funding depth — a combination that markets typically reward with durable multiple expansion rather than a one-day pop.

The broader BNPL sector also benefits. When a pension of CPPIB's caliber allocates at this scale to consumer installment receivables, it signals that institutional funding markets remain open and competitive for the asset class — a meaningful read-through for peers navigating their own funding conversations.

What This Means for Traders

AFFRM equity is trading at $68.38, up +3.11% on the day, with the session high at $68.42 — suggesting the market has begun pricing in this announcement but may not have fully digested the multi-year funding implications. The near-term directional bias is bullish: reduced funding risk, higher GMV ceiling, and potential margin improvement are all catalysts for upward earnings revisions. Traders should watch for analyst target-price updates and any management commentary on how this capacity will be deployed in coming quarters.

For sector exposure, PayPal Holdings and Upstart offer secondary read-through plays — not because they share Affirm's exact funding model, but because institutional appetite for BNPL receivables lifts sentiment across consumer-fintech names. The NASDAQ 100 Index has modest indirect exposure given fintech's weight in growth indices. Volatility on AFRM options may compress slightly as funding-risk premium unwinds, which could make directional long exposure via equity CFDs more attractive relative to options for traders seeking cleaner upside.

This is a cross-sector partnership catalyst with a persistence score that extends beyond the initial headline — the structural funding improvement compounds over the facility's multi-year life, supporting a medium-term bullish thesis on AFRM rather than just a short-term trade.

Trade Affirm Holdings, Inc. on CoinUnited.io

Trade AFRM with up to 800xx leverage → | Create Free Account

Frequently Asked Questions

Not necessarily — this is a forward-flow or warehouse-style funding facility, where CPP Investments provides capital to purchase or fund receivables as they are originated. Affirm's direct balance sheet exposure depends on how much first-loss or equity retention it keeps.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.