Quick Links

Berkshire's $8.5B Taylor Morrison Buyout Sets M&A Floor for Entire Homebuilder Sector

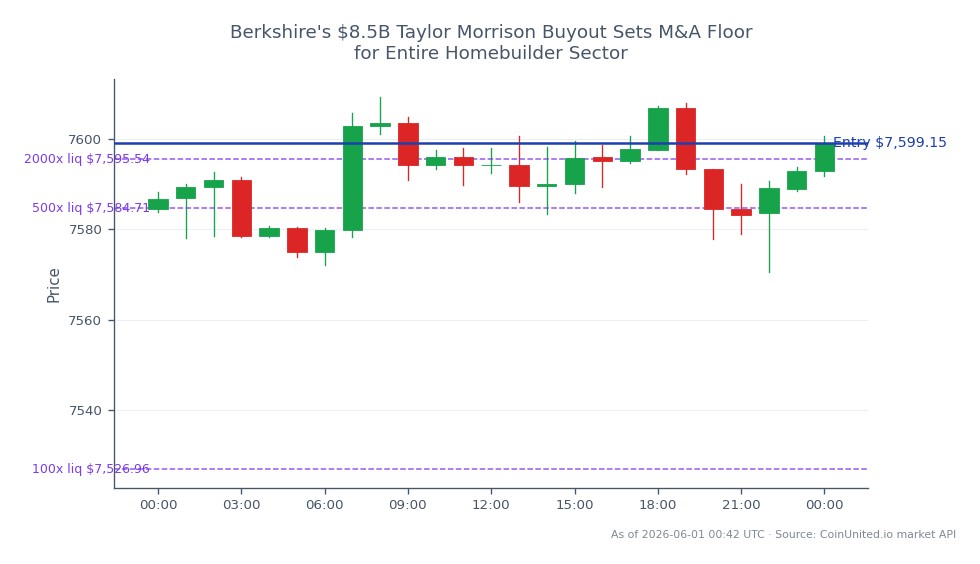

Data Snapshot

Key Takeaways

- •Berkshire Hathaway agreed to acquire Taylor Morrison for $72.50/share cash — a 24% premium to the $58.50 last close — implying $6.8B equity value and $8.5B enterprise value.

- •Leveraged long TMHC CFD traders see amplified gains (24% price move × leverage multiple), while short positions with 10x+ leverage face liquidation risk on the gap.

- •The 24% premium establishes a valuation benchmark for peer homebuilders (DHI, LEN, PHM), supporting sector-wide re-rating and potential M&A speculation premium.

- •Cross-market impact is equity-centric; gold, forex, and crypto see negligible direct spillover from this domestically-focused, USD all-cash deal.

- •Key risk: deal-completion uncertainty (shareholder vote + regulatory approvals) keeps a spread between current market price and $72.50 — that spread is the merger-arb trade until H2 2026 close.

Berkshire Hathaway has signed a definitive agreement to acquire Taylor Morrison Home Corporation (NYSE: TMHC) for $72.50 per share in cash, representing a 24% premium to TMHC's May 29, 2026 closing pr

Event Summary

Berkshire Hathaway has signed a definitive agreement to acquire Taylor Morrison Home Corporation (NYSE: TMHC) for $72.50 per share in cash, representing a 24% premium to TMHC's May 29, 2026 closing price of $58.50, according to the official investor announcement. The deal implies a total equity value of approximately $6.8 billion and a total enterprise value of $8.5 billion. The transaction is expected to close in H2 2026, subject to TMHC shareholder approval and standard regulatory clearances. Upon close, Taylor Morrison will be taken private and delisted from the NYSE.

As reported by HousingWire, this is an all-cash transaction — no stock component — underscoring Berkshire's liquidity strength and conviction in U.S. housing fundamentals at current rate levels. This deal fits squarely within the broader M&A acquisition wave reshaping equity markets in 2026.

Leverage Impact Analysis

For traders running leveraged TMHC CFD positions on CoinUnited.io, the mechanics are straightforward but require careful management.

Long-side scenario: A trader who opened a 20x long TMHC CFD at $58.50 now holds a position worth approximately 24% more at the $72.50 deal price — a ~480% return on margin (24% move × 20x leverage). The key risk is deal spread compression: if TMHC opens near $71.00 rather than $72.50, the remaining $1.50 spread is merger-arb territory, not a momentum trade.

Short-side danger: Any trader short TMHC at sub-$60 levels with 10x or greater leverage faces a margin call or liquidation on the 24% gap up. At 20x short, a 5% adverse move consumes the full margin buffer — a 24% move is catastrophic without stop-loss protection. Monitor open interest for confirmation of short-squeeze dynamics.

The cross-sector acquisition repricing theme means peer homebuilder stocks (D.R. Horton, Lennar, PulteGroup) may also gap — creating secondary leverage risk for traders running sector-spread positions.

Cross-Market Impact

This deal is equity-centric, but the ripple effects span multiple asset classes:

Homebuilder Stocks: The 24% takeover premium functions as a valuation anchor for peers. Traders should watch D.R. Horton (DHI), Lennar (LEN), and PulteGroup (PHM) for sympathy moves — this media & homebuilder acquisition surge signals sector re-rating. Homebuilder ETFs (ITB, XHB) are the cleanest sector-wide expression.

BRK.B: Berkshire deploys $6.8B equity into a rate-sensitive, cyclical sector — a strategic signal, not a financial windfall. BRK.B impact is sentiment-driven; the deal size is manageable relative to Berkshire's overall balance sheet.

S&P 500 Index: Index-level impact from TMHC's eventual delisting is minor given TMHC's mid-cap weight. Broader read-through is bullish for the construction and materials sub-sectors within the US500.

Gold: No direct link. The deal reinforces a risk-on, growth-positive narrative — marginally negative for safe-haven flows into gold in the near term.

Forex/Crypto: Negligible direct impact. The transaction is USD-denominated and domestic. Crypto has no structural connection to this event.

Trading Considerations

TMHC's price should compress toward the $72.50 deal price, with any remaining spread reflecting deal-completion probability and time value to H2 2026 close. Key risk events to monitor: TMHC shareholder vote timeline and any antitrust review updates. For traders interested in the acquisition arbitrage angle, the spread between current market price and $72.50 is the tradeable variable — tighter spreads imply higher deal confidence.

For the sector re-rating trade, watch whether peer homebuilders sustain a bid above pre-announcement levels over the next 5–10 sessions, as this will confirm whether the mega-deal cross-sector acquisition wave is driving genuine valuation uplift or a one-day sympathy pop.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

A 20x long TMHC CFD opened at $58.50 delivers approximately 480% return on margin as the stock reprices toward $72.50. Conversely, any short position with 10x or greater leverage faces near-certain liquidation on a 24% adverse move.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.