Quick Links

Xiaomi Q1 Earnings Miss: Memory Cost Squeeze Opens Leverage Trades Across Chip and Consumer-Tech Stack

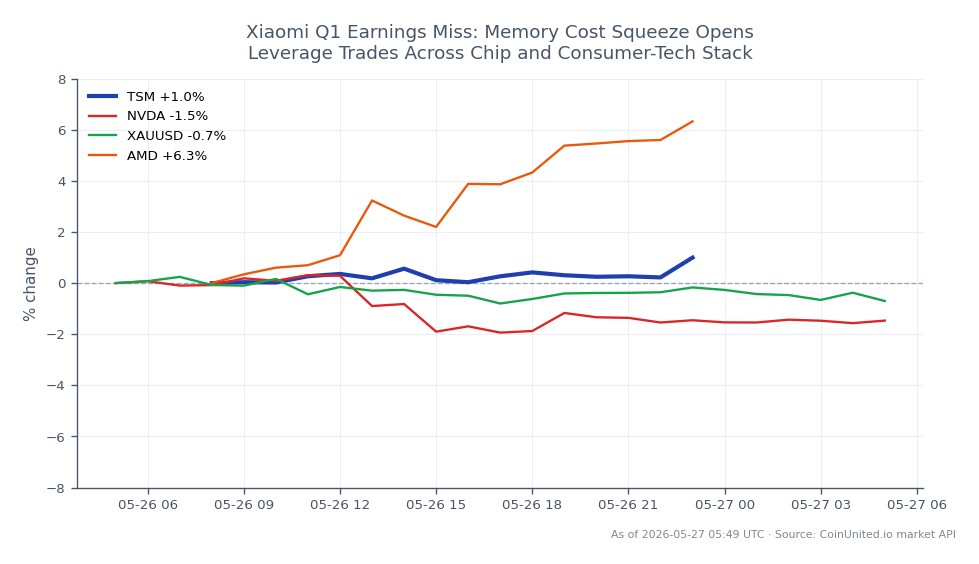

Data Snapshot

Key Takeaways

- •Xiaomi Q1 adjusted net profit missed LSEG consensus by CNY 0.3bn (CNY 6.1bn vs CNY 6.4bn expected), with reported profit down 57% YoY to CNY 4.72bn.

- •Smartphone gross margin collapsed to 10.1% from 12.4% a year ago — the core lever for any re-rating is memory price stabilization, not Xiaomi-specific execution.

- •Leveraged long CFD positions on 1810.HK face compounding risk: 24% YTD drawdown plus unresolved earnings-revision cycle; size leverage accordingly (10x–20x with hard stops).

- •Cross-market read: Xiaomi's pain is NVIDIA, AMD, and TSMC's gain — memory pricing power has shifted structurally to suppliers, supporting the AI chip demand cycle through at least late 2027 per Counterpoint Research.

- •China consumer-tech weakness adds marginal pressure to CNH and Hang Seng Tech constituents; gold and safe-haven assets benefit modestly from risk-off China sentiment.

As reported by the Economic Times and Morningstar/Dow Jones, Xiaomi Corporation posted a sharp Q1 earnings miss driven by surging memory-chip costs. Adjusted net profit fell 43% year-over-year to CNY

Event Summary

As reported by the Economic Times and Morningstar/Dow Jones, Xiaomi Corporation posted a sharp Q1 earnings miss driven by surging memory-chip costs. Adjusted net profit fell 43% year-over-year to CNY 6.1bn (USD ~899m), missing the LSEG consensus of CNY 6.4bn. On a reported basis, net profit dropped 57% to CNY 4.72bn versus analyst expectations of CNY 5.64bn. Revenue declined 11% YoY to CNY 99.14bn, marginally below the CNY 99.52bn consensus.

Smartphone gross margin compressed to 10.1% from 12.4% a year ago, with Xiaomi explicitly attributing the squeeze to higher memory component prices and intensified competition in China. Xiaomi's Hong Kong-listed shares (1810.HK) closed 0.8% lower on the day and are down approximately 24% year-to-date. Counterpoint Research, cited by the Economic Times, expects the memory chip crunch to persist until late 2027.

Leverage Impact Analysis

This earnings miss and revenue shock creates asymmetric risk for leveraged positions in Xiaomi CFDs. Consider a trader holding a 50x long CFD on 1810.HK entered near recent levels — a further 2% decline would wipe 100% of margin. With the stock already down ~24% YTD and earnings-revision risk unresolved, leveraged longs face a structurally challenging environment until memory prices show signs of peaking.

For short-side CFD traders, the risk is a mean-reversion squeeze if any macro catalyst (e.g., a memory price rollover signal or China stimulus announcement) sparks a relief rally. At 50x short, even a 2% bounce erases margin. Given the earnings miss guidance and cost-cycle narrative, moderate leverage (10x–20x) with defined stop-losses above recent resistance is a more calibrated approach than maximum leverage plays. Monitor open interest on 1810.HK for confirmation of directional conviction.

Cross-Market Impact

The memory-cost narrative carries direct read-throughs across multiple asset classes. For NVIDIA and AMD, the signal is paradoxically bullish — Xiaomi's margin pain confirms pricing power has shifted decisively to memory and advanced chip suppliers, supporting the AI revenue and chip demand surge thesis. Taiwan Semiconductor Manufacturing Company benefits from sustained AI-driven wafer demand upstream.

For gold, weak China consumer tech data adds a marginal weight to the bearish-CNH, risk-off-China narrative, which historically nudges flows toward safe-haven assets. The broader semiconductor supply chain geopolitics theme is reinforced — AI-driven memory scarcity is not a short-cycle event, and Counterpoint Research's late-2027 crunch timeline has multi-year portfolio implications. Hang Seng Tech index ETFs with Xiaomi weighting face index-level drag; see the Hang Seng Index trader's guide for broader positioning context.

Trading Considerations

Key levels to watch on 1810.HK: the stock's YTD -24% decline suggests proximity to support zones, but the absence of a near-term catalyst (memory price peak, China demand recovery) limits the upside re-rating case. Earnings-revision cycles for OEMs in margin-squeeze environments typically take 2–3 quarters to stabilize.

For the earnings miss recovery play framework, entry criteria should require external confirmation — a memory price index rollover or a positive China PMI print — rather than valuation alone. Risk factors include further memory cost escalation, CNH weakness amplifying USD-denominated losses, and any EV margin deterioration in Q2 guidance.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

A 50x long CFD on 1810.HK would be fully liquidated on a ~2% further decline; with earnings-revision risk unresolved and the stock already down 24% YTD, high-leverage longs carry outsized downside. Traders should cap leverage at 10x–20x and set stops above identifiable resistance.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.