Quick Links

Honeywell Eyes $2B–$4B M&A Targets as Break-Up Reshapes Deal Strategy

Data Snapshot

Key Takeaways

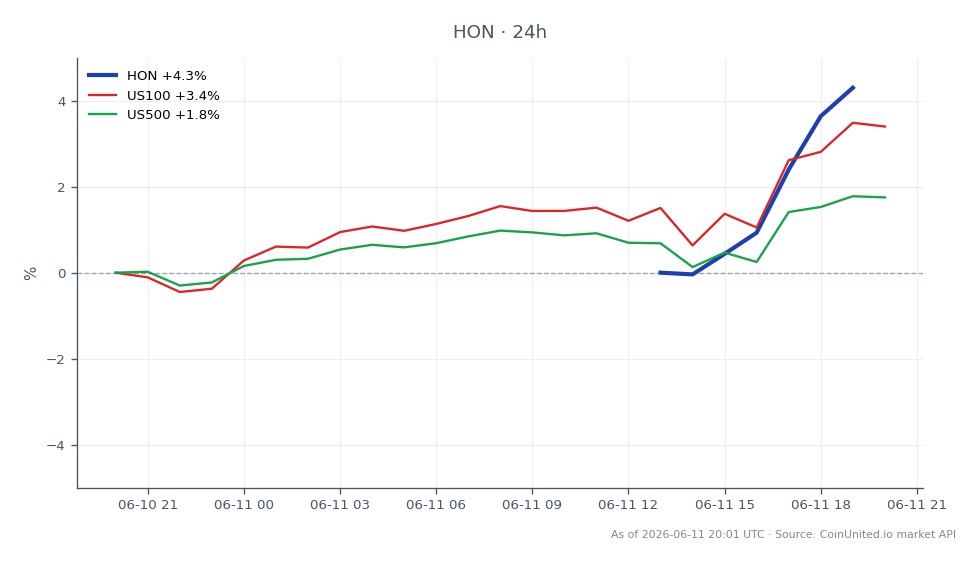

- •HON surged +6.29% to $219.09, reflecting market approval of the growth-via-acquisition strategy alongside the corporate break-up narrative.

- •Honeywell's recent deal history (Sundyne ~$2.2B, CAES $1.9B, Air Products LNG $1.8B) validates the $2B–$4B target range as credible management guidance, not speculation.

- •The simultaneous three-way corporate split means M&A is being used to shape standalone entity profiles — raising the strategic importance of each acquisition beyond simple growth.

- •Industrial peers in automation and aerospace (Emerson, Eaton) warrant monitoring for competitive or sympathy repricing as Honeywell's deal targeting becomes clearer.

- •Index-level impact is modest; this remains a single-stock and industrial-sector catalyst rather than a macro event.

Honeywell International has signaled aggressive acquisition appetite, targeting deals in the $2B–$4B range as management described seeing "a ton of opportunity for M&A." This commentary lands against

Event Analysis

Honeywell International has signaled aggressive acquisition appetite, targeting deals in the $2B–$4B range as management described seeing "a ton of opportunity for M&A." This commentary lands against a backdrop of confirmed recent transactions: the approximately $2.2B acquisition of pump maker Sundyne, $1.9B for CAES Systems Holdings, $1.8B for Air Products' LNG technology business, and $2.4B for Johnson Matthey catalyst technologies, according to reporting from Manufacturing Dive and the Charlotte Observer. The pattern is deliberate — deals clustering around industrial technology, energy security, aerospace, and energy-transition assets.

What makes this cycle structurally different from prior Honeywell acquisition waves is the simultaneous corporate break-up underway. Honeywell is separating into three standalone entities spanning automation, aerospace, and advanced materials. M&A is now a tool not just for growth, but for shaping the eventual standalone profiles of each spinco before separation. Acquisitions completed today will determine the competitive positioning and valuation multiples of tomorrow's independent companies — raising the strategic stakes of every deal announcement.

The M&A acquisition wave theme is well-established in 2026, and Honeywell's posture fits squarely within the broader cross-sector acquisition repricing dynamic where large industrials use balance sheet strength to consolidate niche capabilities ahead of potential re-rating. The Sundyne deal specifically — with its global footprint, ~1,000 employees, and recurring aftermarket revenue — illustrates Honeywell's preference for targets with embedded service streams rather than pure capital-goods exposure.

What This Means for Traders

HON shares are already pricing in positive sentiment, trading at $219.09 (+6.29% over 24 hours, per live market data), with an intraday high of $219.46. The move suggests the market is rewarding the growth-by-acquisition narrative, particularly as deal targets appear accretive within the energy and industrial automation verticals. For traders, the key question is whether the current price reflects near-term deal speculation or a more durable re-rating tied to the break-up value unlock — the latter implies a longer holding thesis. Guidance from management about deal size ($2B–$4B) removes some uncertainty around balance sheet risk, keeping sentiment constructive.

At the sector level, peers in industrial automation and aerospace are worth monitoring for sympathy moves or competitive repositioning signals. Companies like Emerson Electric and Eaton Corporation operate in overlapping verticals and could either benefit from sector re-rating or face increased competitive pressure if Honeywell acquires capabilities in adjacent markets. The energy, pharma & tech M&A wave context also suggests that deal targets in compressors, catalysts, and industrial software may see sentiment-driven upside as Honeywell's consolidation intent becomes clearer. Broad index impact via the S&P 500 is marginal but positive, given HON's weight in the industrials sector.

Trade Honeywell International Inc. on CoinUnited.io

Frequently Asked Questions

It is strategic guidance, not a signed transaction. However, Honeywell's recent track record of closing multiple $1.8B–$2.4B deals gives the commentary credibility as forward intent rather than aspirational talk.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.