Quick Links

Energy-Driven PCE Hits 3-Year High: Leverage Map for WTI at $91.85, USD, and Cross-Market Risk-Off Repricing

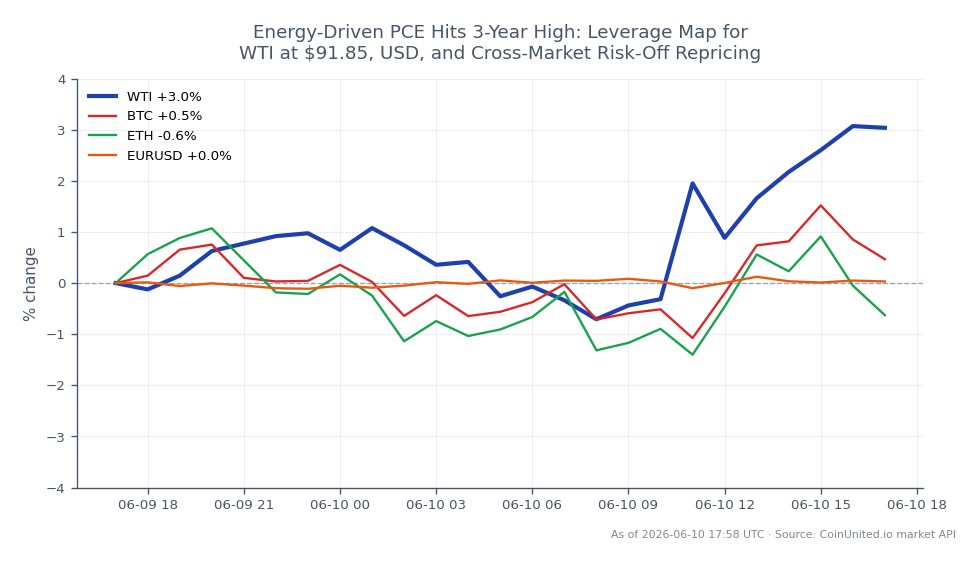

Data Snapshot

Key Takeaways

- •PCE inflation reached 3.8% YoY in April (highest since May 2023), driven by energy commodities up 29.2% YoY and fuel oil +54.3% YoY — not a transitory blip.

- •WTI is trading at $91.85 (+2.34%); leveraged long WTI CFD traders should note the $88.28 session low as the primary stop reference — a -3.9% move from current levels is sufficient to liquidate ~25x positions opened near the high.

- •The Iran conflict + Strait of Hormuz disruption + active U.S. sanctions create a durable geopolitical risk premium in oil, not just event-driven volatility — short positions above $90 carry structural squeeze risk.

- •Cross-market: 'Higher for longer' Fed repricing is bearish for Nasdaq/tech CFDs via multiple compression and bearish for crypto near-term, while supporting USD and energy-linked FX (CAD, NOK).

- •The single relief valve for risk assets is an Iran de-escalation or Hormuz normalization — watch for any diplomatic signals that could rapidly unwind the energy premium and re-open the door to Fed cuts.

U.S. inflation has surged to its highest level in nearly three years, with the PCE price index — the Federal Reserve's preferred gauge — rising 3.8% year-on-year in April, the highest reading since Ma

Event Summary

U.S. inflation has surged to its highest level in nearly three years, with the PCE price index — the Federal Reserve's preferred gauge — rising 3.8% year-on-year in April, the highest reading since May 2023, according to U.S. Commerce Department data. Monthly PCE came in at +0.4% MoM, easing from March's 0.7% but still well above comfort levels.

The driver is unambiguous: energy. U.S. energy inflation hit 17.9% YoY in April — the steepest annual increase since September 2022 — with energy commodities up 29.2% YoY, gasoline +28.4% YoY, and fuel oil surging +54.3% YoY. Officials and analysts attribute the spike to the Iran conflict, disruption risk at the Strait of Hormuz, and fresh U.S. sanctions targeting Iranian crude exports. The U.S. Treasury has explicitly stated it will "not allow Tehran to boost oil revenues," signaling sustained supply constraint.

Analysts cited in coverage note that without a reversal in energy prices, inflation is likely to remain elevated — pushing the Fed toward a "higher for longer" posture well into next year.

Leverage Impact Analysis

WTI Light Crude Oil is currently trading at $91.85, up +2.34% on the session (24h high: $92.71 / low: $88.28), confirming the market is actively pricing this inflation print.

Long WTI CFD scenarios at current levels:

- -A 50x long WTI CFD opened at $91.85 sees ~$10.77 gain per contract on today's +2.34% move. A 2% adverse reversal to ~$90.00 would erase roughly half that margin buffer — position sizing matters here.

- -A 100x long WTI CFD opened at $91.85 amplifies that same 2% swing to a ~23.5% margin impact. The $88.28 session low represents the nearest hard risk reference: a flush to that level from current price is a -3.9% move, sufficient to liquidate ~25x+ long positions opened near today's high without adequate margin.

Short-side risk: Traders short WTI on a "buy the rumor, sell the news" thesis face a structural problem — the geopolitical premium (Iran/Hormuz) is not event-driven noise but a stagflation risk and geopolitical inflation shock with policy backing. Shorts above $90 carry squeeze risk if Hormuz disruption escalates.

For broader macro inflation risk-off repricing, leveraged longs in rate-sensitive assets (Nasdaq CFDs, long-duration bond proxies) face the most asymmetric downside: a "higher for longer" Fed repricing compresses multiples faster than headline indices reflect.

Cross-Market Impact

Commodities: Brent Crude Oil and Gasoline follow WTI's lead with structurally embedded geopolitical premium. Natural Gas benefits modestly via electricity (+6.1% YoY) and piped gas (+3.0% YoY) pass-through. Gold (XAU/USD) faces a split signal: higher real yields are a headwind, but persistent inflation supports the inflation hedge asset rotation bid — net effect likely range-bound with upside skew if risk-off deepens.

Forex: "Higher for longer" Fed is USD-supportive. EUR/USD faces downward pressure if the ECB diverges on pace — our Fed vs. ECB macro policy divergence guide covers this dynamic in depth. USD/JPY is at risk of further yen weakness given Japan's energy import exposure, though intervention risk caps the move. Commodity FX (CAD, NOK) finds modest support.

Equities/Indices: The NASDAQ 100 is the most exposed index via duration sensitivity — tech multiple compression accelerates when terminal rate expectations ratchet higher. The S&P 500 sees sector rotation: energy outperforms, consumer discretionary and REITs underperform. Airlines (fuel cost squeeze) are notable sector risk — see our United Airlines trader's guide.

Crypto: Near-term, tighter financial conditions and higher real yields pressure Bitcoin and Ethereum. Medium-term, sticky inflation reinforces BTC's "digital gold" narrative for patient holders. Monitor funding rates on CoinUnited.io for leverage sentiment signals.

Trading Considerations

WTI's session range ($88.28–$92.71) defines near-term risk parameters. The $88.28 low is the first meaningful support; a break below that level would signal demand exhaustion and trigger long liquidations across leveraged positions. Resistance clusters near the $92.71 session high, with a sustained break opening the path toward the $95+ zone if Hormuz risk escalates further.

The key variable to watch is energy supply normalization: any credible Iran de-escalation signal or Hormuz stabilization would rapidly deflate the geopolitical premium, reverse the inflation narrative, and benefit rate-sensitive longs (Nasdaq, crypto, long bonds). Until then, the Fed macro policy crossroads bias favors energy longs and USD strength over growth assets.

Trade WTI Light Crude Oil on CoinUnited.io

Trade WTI with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

WTI is at $91.85 with the session low at $88.28 — a -3.9% gap that defines liquidation risk for positions above ~25x leverage opened near the high. The geopolitical premium (Iran/Hormuz) provides structural support, but position sizing relative to that $88.28 floor is critical.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.