Quick Links

SailPoint Guidance Shock: EPS and Revenue Targets Fall Short, Raising SaaS Growth Questions

Data Snapshot

Key Takeaways

- •SailPoint guided Q1 FY26 revenue at $273–$277M vs. $280.8M consensus — a miss that triggered multiple analyst price-target cuts.

- •FY2027 adjusted EPS guidance of $0.30–$0.34 fell below Street forecasts, compressing long-duration growth valuations and driving an ~12% single-day drop.

- •Q2 EPS guidance of $0.07–$0.08 only reaches consensus at the top end, offering no upside surprise buffer for investors.

- •The multi-layer miss (near-term revenue, near-term EPS, long-term EPS) is more damaging than a single-metric disappointment for a premium-multiple SaaS name.

- •Whether this is idiosyncratic or a sector signal depends on upcoming peer results in IAM and enterprise cybersecurity — watch those prints closely.

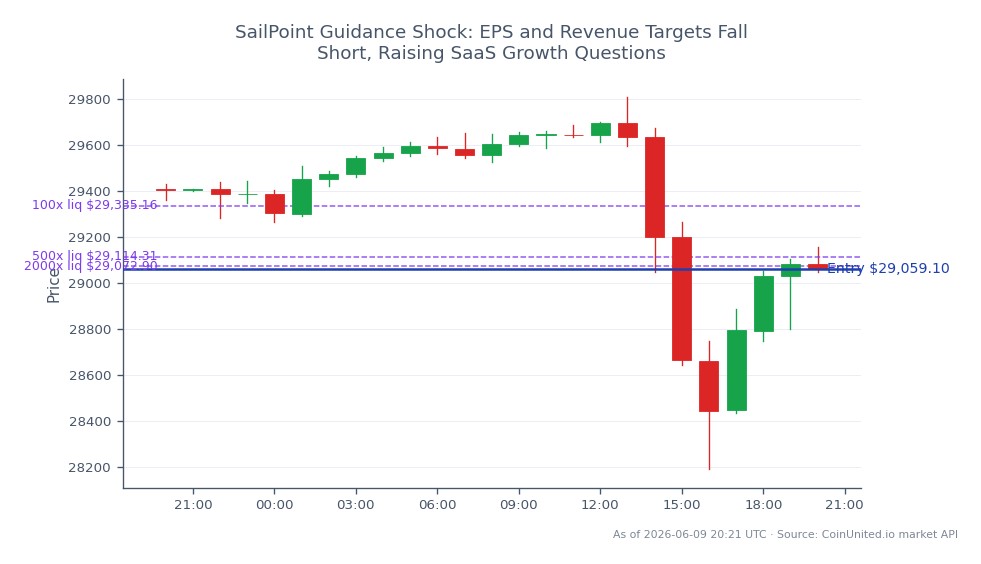

SailPoint Technologies (SAIL) delivered a guidance package that fell short of Wall Street's expectations across multiple dimensions, triggering immediate share price pressure. As reported by Investing

Event Analysis

SailPoint Technologies (SAIL) delivered a guidance package that fell short of Wall Street's expectations across multiple dimensions, triggering immediate share price pressure. As reported by Investing.com, the company posted a significant quarterly earnings miss and followed with Q2 EPS guidance of $0.07–$0.08 per share — only touching the Street consensus of $0.08 at the very top of the range. More damaging was Q1 FY26 revenue guidance of $273–$277 million versus analyst expectations of $280.8 million, which Stocktwits coverage characterized as "underwhelming" and prompted multiple analyst price-target cuts. Longer-dated guidance compounded the pressure: FY2027 adjusted EPS of $0.30–$0.34 came in below forecasts, directly pressuring discounted cash flow models that underpin SailPoint's growth-premium valuation.

This miss matters beyond the individual numbers. SailPoint operates in identity and access management (IAM) — one of cybersecurity's most defensible and budget-resilient niches. When even IAM names guide conservatively, it raises uncomfortable questions about enterprise security spending velocity. As noted by Tickeron, shares dropped approximately 12% on the FY2027 EPS disappointment, a reaction that signals investors had priced in an acceleration that management is no longer willing to endorse. For a sector where valuation multiples are justified by compounding ARR growth, a guided ARR range of $1.218–$1.222 billion that merely brackets rather than beats consensus erodes the premium.

What differentiates this from routine SaaS guidance conservatism is the multi-layer nature of the miss: near-term EPS, near-term revenue, and long-duration EPS all missed or only matched expectations simultaneously. MarketBeat analysis does note that SailPoint's underlying fundamentals — consistent prior beats, ARR trajectory — remain intact, suggesting this could be conservative guidance rather than structural deterioration. That ambiguity is precisely what creates a two-sided trading setup. Investors must now determine whether management is resetting the bar defensively or genuinely signaling a slower growth phase ahead.

What This Means for Traders

The immediate bias for SAIL is bearish in the near term, consistent with the earnings miss revenue shock playbook. Guidance misses in high-multiple SaaS names typically produce a valuation compression phase as analysts revise price targets and institutional models are adjusted — a process that plays out over days to weeks, not hours. Traders considering the contrarian earnings miss recovery angle should wait for stabilization signals: flat-to-recovering ARR commentary, peer confirmation that enterprise security budgets remain healthy, or a clear floor in analyst revisions.

For sector positioning, the key question is whether this miss is idiosyncratic or a read-through for broader cybersecurity/software spending. If subsequent peer results in identity management or zero-trust security come in strong, SAIL's weakness becomes a pair-trade opportunity. If peers echo similar caution, the earnings miss guidance cuts dynamic could weigh on the wider software complex. Traders monitoring the S&P 500 and NASDAQ 100 should note that high-multiple tech names remain sensitive to any pattern of guidance disappointment — SAIL's reaction could amplify risk-off pressure on growth-factor exposure if it becomes a trend rather than an outlier.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

Current analyst framing leans toward company-specific execution and conservative guidance rather than a broad sector breakdown, but confirmation requires watching peer IAM and cybersecurity earnings prints over coming weeks.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.