Quick Links

TCS Faces $220M Final Judgment as U.S. Supreme Court Rejects Trade Secrets Appeal

Data Snapshot

Key Takeaways

- •The U.S. Supreme Court denied TCS's appeal, making the $220M Epic Systems judgment legally final with no further recourse.

- •The earnings impact depends critically on prior provisioning — inadequate provisions mean a negative EPS surprise; full provisions mean risk removal.

- •TCS's heavy weighting in the Nifty 50 and Sensex means stock-specific weakness can drag broader Indian equity benchmarks.

- •Indian IT sector peers face indirect sentiment pressure as investors reassess IP compliance risk across the space.

- •Cross-border enforcement actions of this scale reinforce a structural theme: U.S. courts are willing to impose nine-figure penalties on foreign tech firms for trade-secret violations.

According to Investing.com, Tata Consultancy Services (TCS) — India's largest IT services company by market capitalization — will pay $220 million to Epic Systems Corporation after the U.S. Supreme Co

Event Analysis

According to Investing.com, Tata Consultancy Services (TCS) — India's largest IT services company by market capitalization — will pay $220 million to Epic Systems Corporation after the U.S. Supreme Court denied certiorari, refusing to hear TCS's appeal in a long-running trade secrets misappropriation case involving Epic's healthcare software. The Supreme Court's denial is procedurally final: no further federal appeal is possible, transforming what was a contingent legal liability into a confirmed cash outflow.

The significance here lies in finality. Markets can tolerate uncertainty; what they price imprecisely is unresolved litigation. This ruling removes that ambiguity entirely. The critical unknown now is how much TCS had already provisioned against this liability in prior quarters. If provisions fall materially short of $220 million, the incremental charge represents a genuine negative earnings surprise. If TCS had conservatively pre-provisioned closer to the full amount, the news paradoxically functions as a risk-removal event — eliminating overhang rather than introducing new damage.

Beyond TCS's balance sheet, this ruling carries sector-wide signaling value. This case fits squarely within the cross-border enforcement repricing pattern, where U.S. courts impose material financial penalties on large foreign technology firms for IP and trade-secret violations. Combined with the broader global regulatory enforcement wave reshaping how markets price legal risk at multinational tech companies, investors in Indian IT services peers — Infosys, Wipro, HCLTech — may revisit their own IP compliance risk premiums, even absent direct exposure to this specific case.

What This Means for Traders

For TCS equity traders, the immediate question is provisioning coverage. A confirmed $220 million outflow is meaningful relative to quarterly net profit for even a large-cap IT services firm; it can compress near-term EPS, reduce free cash flow available for buybacks or dividends, and prompt modest multiple de-rating if investors view this as symptomatic of weaker internal controls. Conversely, management commentary confirming adequate prior provisioning could see TCS shares stabilize or recover quickly on the removal of legal uncertainty. Monitoring the India NIFTY 50 Index and India S&P BSE SENSEX is warranted given TCS's heavyweight index presence — a sustained TCS move will drag or support these benchmarks.

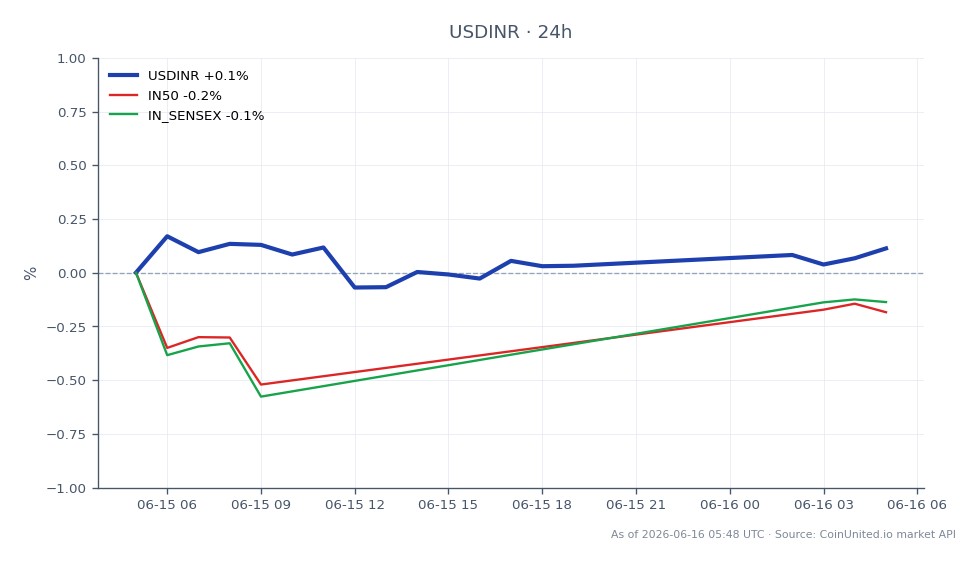

The cross-market effect on the US Dollar / Indian Rupee is negligible; a $220 million cross-border flow is immaterial against daily FX volumes. Sector read-across is the more relevant transmission channel: Indian IT ETFs and funds with concentrated TCS exposure could underperform broader India benchmarks in the short term. This is a stock-specific, idiosyncratic event with contained but real sector spillover — not a macro repricing catalyst.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

No. A U.S. Supreme Court denial of certiorari is procedurally final at the federal level — TCS has exhausted all U.S. appellate options and must pay the judgment.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.