Quick Links

GSK Acquires IDRx for $1.15B in Biggest Oncology Deal in Eight Years — Leverage Scenarios & Sector Read-Through

Data Snapshot

Key Takeaways

- •GSK is paying $1.0B upfront ($1.15B total) for IDRx — its largest oncology acquisition since divesting its cancer portfolio to Novartis ~8 years ago, signalling a strategic pivot back to GI oncology.

- •LEVERAGE: A 50x long GSK CFD at $50.70 faces liquidation on a ~2% drawdown (~$49.69); the post-deal dip to $50.45 intraday shows the risk window is active — tight stops are essential.

- •Royalty obligations owed to Merck KGaA on IDRX-42 compress GSK's long-term gross margin on the asset — an underappreciated risk in the deal economics.

- •CROSS-MARKET: The $1B+ oncology price tag is a positive read-through for clinical-stage precision oncology and GI cancer biotech peers (GIST/GI tumor names), increasing perceived takeout premiums sector-wide.

- •No macro, FX, commodity, or crypto spillover is identifiable — this is a pharma sector-specific event.

According to GSK's official press release, GSK plc (NYSE: GSK) has entered into a definitive agreement to acquire 100% of IDRx, Inc., a Boston-based clinical-stage biopharmaceutical company focused on

Event Summary

According to GSK's official press release, GSK plc (NYSE: GSK) has entered into a definitive agreement to acquire 100% of IDRx, Inc., a Boston-based clinical-stage biopharmaceutical company focused on precision therapies for gastrointestinal stromal tumors (GIST). The deal comprises $1.0 billion in upfront cash plus up to $150 million in contingent regulatory milestone payments, totalling $1.15 billion maximum consideration — GSK's largest oncology acquisition in approximately eight years.

IDRx's lead asset, IDRX-42, targets GIST, a high-unmet-need niche in GI oncology. Notably, GSK will inherit success-based milestone payments and tiered royalties owed to Merck KGaA, Darmstadt, Germany on IDRX-42 — a royalty overhang that modestly compresses future gross margin potential. This deal marks GSK's deliberate strategic rebuild of oncology scale M&A following its ~$16 billion oncology portfolio divestiture to Novartis around 2015.

Leverage Impact Analysis

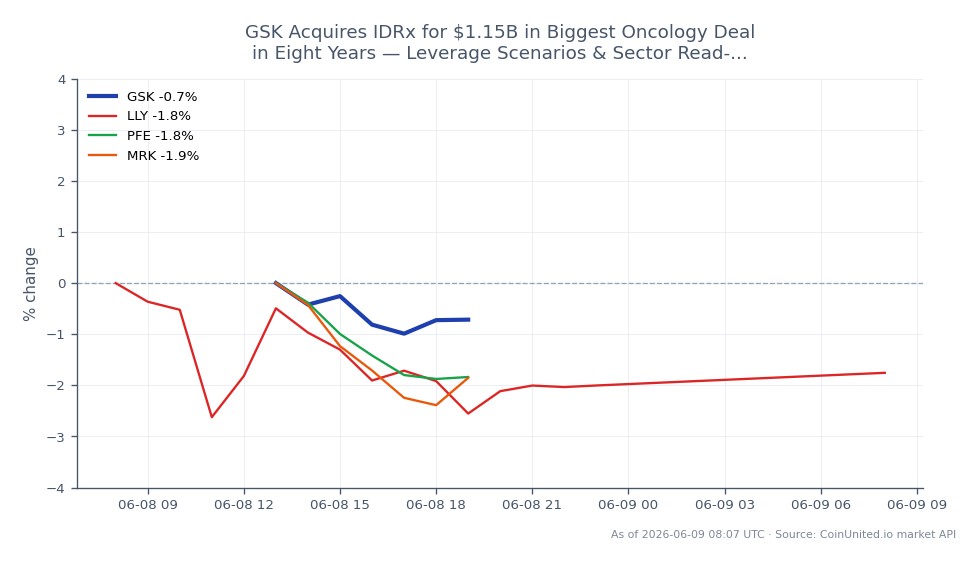

GSK is currently trading at $50.70 (24h range: $50.45–$51.39, down 1.69%), suggesting the market has partially absorbed the announcement with some initial caution — a pattern common in acquirer-side M&A where cash outflow concerns offset pipeline optimism. This creates a two-sided leverage opportunity.

Long scenario: A trader opening a 50x long GSK CFD at $50.70 on CoinUnited.io controls $253,500 in notional exposure per $5,070 margin. A recovery to the 24h high of $51.39 (+1.36%) generates ~$685 in P&L — a 68% return on margin. However, a further 2% decline to ~$49.69 would trigger liquidation on a 50x position, illustrating the tight margin for error on acquirer-side M&A plays.

Short scenario (fading the deal): If the market reprices the $1.0B cash outflow as a negative for near-term capital returns (dividends/buybacks), a 50x short from $50.70 profits ~$34 per $1.01 move lower. Key downside watch: loss of buyback guidance or analyst target cuts post-deal would be the trigger.

For traders using the broader M&A acquisition wave playbook, acquirer stocks historically underperform in the 3–5 days post-announcement before pipeline NPV models stabilize sentiment. Position sizing discipline is critical — monitor for analyst commentary and any guidance revision before scaling leverage.

Cross-Market Impact

This deal slots directly into the energy, pharma & tech acquisition wave theme reshaping healthcare sector valuations. The primary read-through is positive for clinical-stage oncology biotech peers — large pharma paying $1B+ for a pre-revenue GIST asset signals continued willingness to acquire precision oncology platforms at premium multiples.

Peer implications: Merck & Co., Inc. competes in oncology (Keytruda) and faces indirect competitive pressure as GSK rebuilds its GI cancer portfolio. Bristol-Myers Squibb Company and Eli Lilly and Company may see valuation re-ratings as analysts assess who is under-invested in precision oncology. Pfizer, Inc. has its own GI oncology exposure and could be drawn into comparative M&A catch-up discussions.

The deal is micro/sector-specific with no material macro spillover — no FX, rates, commodities, or crypto impact is identifiable given the $1B deal scale relative to global capital markets.

Trading Considerations

Key levels: GSK's 24h low of $50.45 acts as immediate support; a break below opens a test of broader technical support. Resistance sits at the 24h high of $51.39. The current price of $50.70 sits near the lower end of the day's range, suggesting post-announcement selling pressure has not fully resolved.

Watch for: (1) analyst price target revisions in the 24–48 hours post-announcement; (2) any guidance commentary on capital returns — the pharma & fintech acquisition repricing theme suggests acquirer stocks often re-rate once deal NPV models are published. The royalty overhang to Merck KGaA on IDRX-42 is an underappreciated margin risk worth monitoring.

Trade GSK plc on CoinUnited.io

Frequently Asked Questions

At $50.70 with a 24h low of $50.45, a 50x long GSK CFD is operating within a ~0.5% buffer from that intraday support — a further 2% decline liquidates the position. Traders should size conservatively and await analyst NPV model publications before adding leverage.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.