Quick Links

Allied Gold Drops as C$5.5B Zijin Deal Faces China Regulatory Risk — M&A Arb in Focus

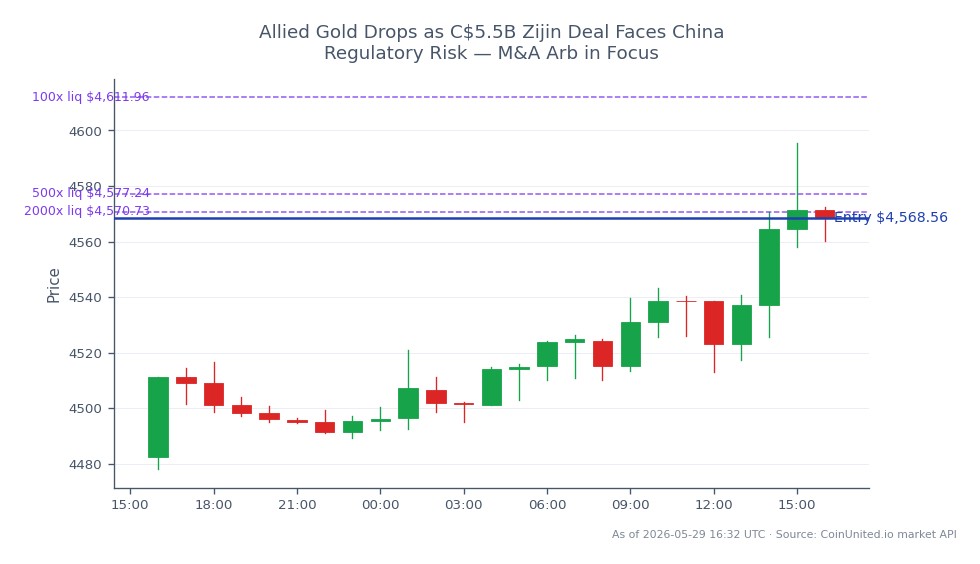

Data Snapshot

Key Takeaways

- •Allied Gold (AAUC) trades below the C$44.00 offer price as markets reprice Chinese regulatory approval risk — the core variable for all leveraged positions.

- •Leverage warning: A 20x long AAUC CFD sees ~200% margin loss on a 10% drop from offer price — deal-arb requires smaller position sizing than directional trades.

- •Zijin's listed mining entities face strategic growth delay: the deal was intended to boost mined gold output by ~23.5% YoY to 90 tonnes in 2025.

- •Cross-market: Spot gold is largely unaffected in the near term, but African gold mining peers with perceived Chinese-acquirer optionality may see M&A premium compression.

- •Watch for: Official statements from Chinese regulators (MOFCOM/NDRC), changes to Allied's plan of arrangement filing, and AAUC volume relative to C$44 as implied deal-completion odds.

Zijin Gold International, a subsidiary of Zijin Mining Group, announced an all-cash offer to acquire Allied Gold Corporation (AAUC) at C$44.00 per share, valuing the target at approximately C$5.5 bill

Event Summary

Zijin Gold International, a subsidiary of Zijin Mining Group, announced an all-cash offer to acquire Allied Gold Corporation (AAUC) at C$44.00 per share, valuing the target at approximately C$5.5 billion (~US$4.0B) — Zijin's largest acquisition in history, according to official corporate filings. The friendly deal, structured as a Canadian plan of arrangement, carries a roughly 27% premium to Allied's 30-day VWAP prior to announcement.

According to Allied Gold's investor relations disclosures, the transaction remains conditional on Allied shareholder approval, Canadian court sanction, and multi-jurisdictional regulatory clearances — including Chinese authorities. Market reports now indicate the deal faces opposition within China, transforming what appeared a near-certain cash takeout into a live M&A acquisition wave risk-arbitrage scenario.

Leverage Impact Analysis

For leveraged CFD traders on Allied Gold stock, this event creates a binary spread structure. With the offer price anchored at C$44.00 and the stock now trading below that level on deal-break fears, the position risk is highly asymmetric:

- -Long AAUC CFD at 20x leverage: A 10% drop from offer price (to ~C$39.60) generates a 200% loss on margin — effectively a wipe-out. Position sizing must account for the full downside to standalone fundamental value, not just the spread to C$44.

- -Long AAUC CFD at 5x leverage: The same 10% move costs 50% of margin — painful but survivable if the trader has budgeted for deal-break risk.

- -Short AAUC CFD: If the deal is blocked and Allied reverts to pre-deal fundamental valuation (materially below C$44), shorts stand to gain, but face unlimited upside risk if Chinese approval comes through unexpectedly.

This is a classic cross-sector acquisition repricing event. High leverage on either side is dangerous given the binary outcome. Traders should review the acquisition arbitrage guide before sizing positions.

Cross-Market Impact

Gold (XAU/USD): The transaction is a change of ownership, not a supply event — spot gold is unlikely to move on deal outcome alone. However, if Chinese regulatory resistance signals broader tightening of outbound mining acquisitions, the pace of consolidation-driven capex into African gold assets could slow, marginally weighing on gold miner ETF premiums over the medium term.

Zijin Mining (A/H-shares): A blocked deal removes Zijin's path to its >100-tonne annual gold production target and a projected +23.5% YoY volume lift. Zijin's listed vehicles face downside from strategic growth delay and management credibility risk. This feeds into the broader mining and industrial acquisition surge theme.

African gold mining peers: Chinese capital has been a key acquirer of African gold assets. Visible regulatory pushback could widen the implied discount rate applied to other Africa-focused producers listed on the TSX, LSE, and ASX — affecting the sector's M&A premium broadly.

CAD/FX: The C$5.5B all-cash deal represented marginal CAD-supportive FDI inflows. A failed deal removes that marginal support, though the macro FX impact is minimal versus daily FX turnover.

Trading Considerations

The key level is C$44.00 — the ceiling if the deal closes, and a reference for sizing the deal-break discount. Traders should monitor official filings from Allied Gold and Zijin for any regulatory timeline updates or revised terms; any statement from Chinese authorities (MOFCOM, NDRC) is the primary catalyst. Volume and price action in AAUC relative to C$44 will serve as the real-time implied completion probability indicator.

Risk is binary and event-driven. Position sizes appropriate for a deal-arb scenario — where the downside is a revert to standalone NAV — are materially smaller than a directional trade. Refer to CoinUnited.io's live pricing for current spread levels before entering.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

The reported opposition widens the deal spread — AAUC trades below C$44 as markets price in a higher deal-break probability. A leveraged long is now exposed to a binary downside: if the deal fails, AAUC could fall significantly below C$44 toward standalone fundamental value, amplifying losses proportionally to leverage used.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.