Quick Links

Agilent Q2 Earnings Beat Signals Life Sciences Sector Recovery — Stock Surges ~8%

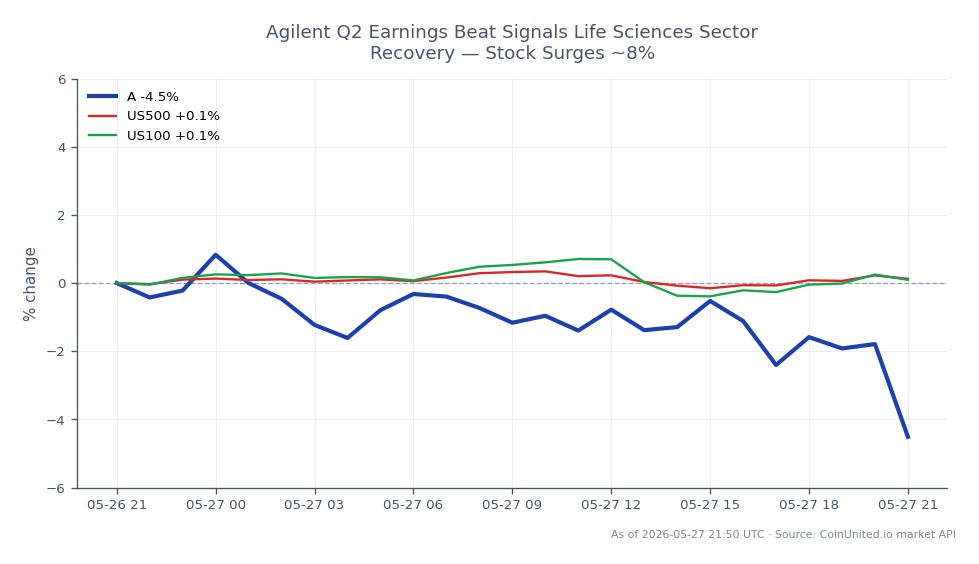

Data Snapshot

Key Takeaways

- •Agilent Q2 EPS of $1.31 beat the $1.26 consensus; revenue grew 6% YoY to $1.67B — marking a fourth straight quarter of accelerating growth.

- •FY2026 adjusted EPS guidance raised to $6.00–$6.10, signaling management confidence that the recovery trend is durable.

- •The ~8% post-earnings surge reflects a genuine sentiment shift in life sciences tools — not just a relief rally.

- •Incremental tariff costs flagged by management are a watch item for sector-wide margin expectations in H2.

- •Positive read-through likely for lab instrumentation and analytical equipment peers; broader index impact is limited.

Agilent Technologies, Inc. (NYSE: A) delivered a clear beat in its fiscal Q2 2026 results, with adjusted EPS of $1.31 versus expectations of $1.26 and revenue of $1.67 billion, representing 6% reporte

Event Analysis

Agilent Technologies, Inc. (NYSE: A) delivered a clear beat in its fiscal Q2 2026 results, with adjusted EPS of $1.31 versus expectations of $1.26 and revenue of $1.67 billion, representing 6% reported and 5.3% core year-over-year growth, according to Investing.com. The quarter marked the fourth consecutive period of accelerating growth, a streak that adds meaningful credibility to management's bullish tone. Operating margin came in at 25.1%, and the company subsequently raised its fiscal 2026 adjusted EPS guidance to $6.00–$6.10, up from a prior range near $5.90–$6.04.

What makes this result strategically significant is the trajectory, not just the beat. Agilent serves a demanding mix of pharma, biotech, industrial testing, and government/academic labs — end markets that were under pressure through 2024 due to destocking cycles and softer research budgets. Four quarters of accelerating growth suggests those headwinds have genuinely cleared, not merely stabilized. This is a meaningful read-through for the broader diversified sector earnings beat wave theme unfolding across analytical instruments and life sciences tools peers.

One notable caveat management flagged: incremental tariff costs. This matters for the sector at large, as many instruments manufacturers carry globally distributed supply chains with import-sensitive components. Traders should watch whether peers absorb similar cost pressures or manage to pass them on — the answer will shape margin expectations across the space. For those seeking a broader framework on earnings beats across sectors, Agilent's result fits a pattern of selective, high-quality beats in capital equipment names.

What This Means for Traders

As reported by Investing.com, Agilent shares surged approximately 8% on the results — a reaction sized for a confirmed demand recovery narrative, not just a routine quarterly beat. The guidance lift adds durability to that move; it's not a one-quarter anomaly but a raised annual bar. Sentiment for life sciences tools peers — think diagnostic instruments, lab automation, and analytical chemistry equipment — can benefit from positive read-through, as Agilent's end-market exposure broadly overlaps with the sector. Traders tracking the S&P 500 Index and NASDAQ 100 Index will note this is sector-specific rather than macro-wide, but it does reinforce a risk-on bias in quality growth names.

This earnings event was reported around May 27, 2026. Since the reaction has likely already been priced into the opening session, the near-term setup shifts toward watching whether momentum holds above the post-earnings gap level or fades as traders take profit. For those using the earnings beat sector playbooks framework, the key question is whether Agilent's raised guidance proves conservative — as it often does in recovery cycles — or whether tariff cost creep begins to compress the margin story in Q3.

Trade Vaulta on CoinUnited.io

Frequently Asked Questions

The magnitude reflects cumulative confidence: four consecutive quarters of accelerating growth plus an upward guidance revision signals a sustained recovery, not a one-off. Markets reward trajectory, not just a single-quarter margin.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.