Quick Links

UK's 78% North Sea Tax Burden: How Fiscal Squeeze Hits WTI at $101.57 and Leveraged Energy Traders

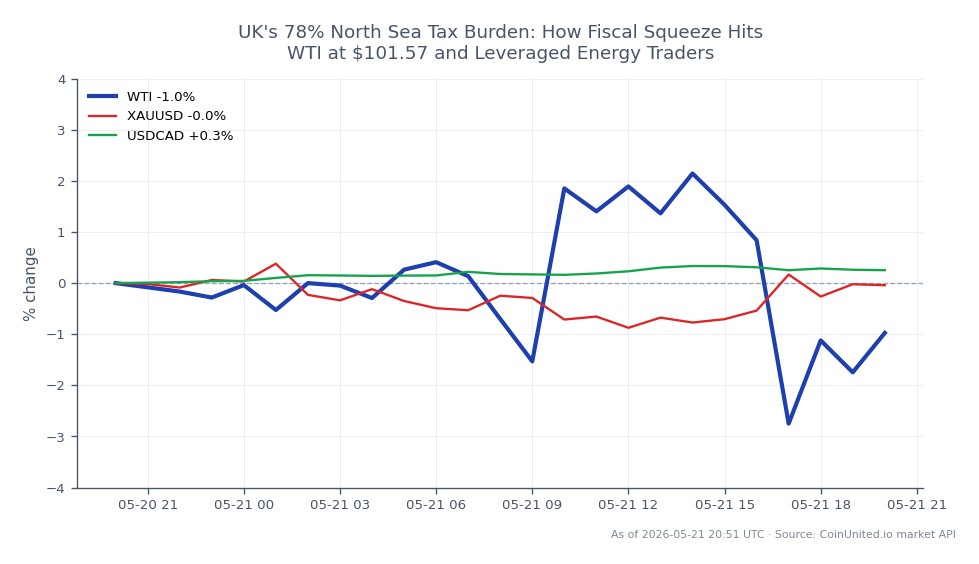

Data Snapshot

Key Takeaways

- •The UK EPL now totals 78% effective tax on North Sea profits (40% permanent + 38% levy), running to March 2028 — the highest sustained marginal rate among major oil basins.

- •Leveraged WTI CFD traders: the live $6.85 daily range ($99.17–$106.02) means a 50x position risks 220%+ margin loss on a full intraday reversal — size accordingly.

- •Capital flight from the UKCS structurally benefits Norway (NOK bullish) and US Gulf of Mexico operators like Chevron and ExxonMobil over UK-centric E&Ps.

- •GBP faces dual pressure: weaker FDI from reduced North Sea investment and potential stagflation dynamics if higher import energy dependency anchors UK inflation.

- •The Brent-WTI spread is the cleaner commodity trade — North Sea supply erosion supports a Brent premium expansion over the medium term.

The UK's Energy Profits Levy (EPL) has been incrementally tightened since its May 2022 introduction at 25%, rising to 35% in January 2023 and subsequently to 38% under the Labour government in Novembe

Event Summary

The UK's Energy Profits Levy (EPL) has been incrementally tightened since its May 2022 introduction at 25%, rising to 35% in January 2023 and subsequently to 38% under the Labour government in November 2024. According to official HM Treasury documents and industry body Offshore Energies UK (OEUK), the total marginal tax rate on UK Continental Shelf (UKCS) oil and gas profits now stands at ~78% — comprising the permanent 40% ring-fenced regime plus the 38% EPL. The levy runs through March 2028, with OEUK estimating it will extract £80 billion from the sector by that date, including £15 billion in the current fiscal year.

A parallel Electricity Generator Levy (EGL) at 45% applies to power sold above £75/MWh, hitting offshore wind, biomass, and gas-fired generators. As reported by Energy In Depth, three years of windfall taxation have "shattered investment confidence, accelerated production decline, and destabilized the North Sea's vital supply chain." INEOS has called for urgent EPL removal to restore competitiveness with US operators.

Leverage Impact Analysis

WTI Light Crude Oil is trading at $101.57 (24h range: $99.17–$106.02, -0.96%). The UK tax story is structurally bearish for UK-exposed producers but its direct WTI price impact is indirect — reduced North Sea capex tightens medium-term Atlantic Basin supply, a mild bullish offset against the near-term demand caution implied by WTI's current pullback from recent highs.

Leverage scenario — WTI CFD short (bearish producer sentiment play):

- -A 50x short WTI CFD opened at $101.57 requires ~$2.03/barrel in margin per contract.

- -A reversal to the 24h high of $106.02 (+4.4%) would generate a 220% loss on margin, triggering liquidation well before that level for positions sized near maximum exposure.

- -Conversely, a move to the 24h low of $99.17 (-2.4%) delivers a +120% return on margin at 50x.

Key risk: WTI remains in a volatile regime (daily range $6.85 on live data). Traders using leverage above 20x on WTI CFDs face liquidation from intraday swings alone — position sizing must account for the full daily range, not just directional conviction. Monitor Brent Crude Oil for spread divergence as North Sea supply concerns could widen the Brent-WTI differential.

Cross-Market Impact

GBP/USD: Structural erosion of North Sea investment reduces UK energy sector FDI inflows and worsens the trade balance over time, adding medium-term downward pressure to GBP/USD. Near-term, BoE policy dominates; the EPL's inflationary pass-through (higher import dependency) could keep rate-cut expectations cautious, limiting GBP downside.

USD/CAD & USD/NOK: The UK's policy instability directly benefits competing basins. Norway, despite comparable headline tax rates, offers greater policy certainty — supporting USD/NOK as NOK gains from redirected North Sea investment flows. Canada's oil sands similarly attract displaced capex, bearish for USD/CAD.

Energy Equities (XOM, CVX): US majors Chevron Corporation and ExxonMobil are net beneficiaries — capital fleeing the UKCS redirects to Gulf of Mexico and international assets where these companies have leverage. Relative outperformance vs UK-centric E&Ps (Harbour Energy, EnQuest) is the cleaner trade expression.

Gold: If UK energy inflation anchors BoE hawkishness while weakening growth, stagflation dynamics emerge — supportive of Gold as an inflation hedge. The macro inflation pressure channel is real but secondary to global supply factors at current WTI levels.

Trading Considerations

WTI at $101.57 sits near the lower bound of its recent $99–$107 range. The North Sea fiscal story is a slow-burn structural theme rather than an acute catalyst — it reinforces medium-term supply tightness but won't spike WTI alone. Key levels to watch: $99.17 (24h low / near-term support), $106.02 (24h high / resistance), with a break below $99 potentially opening a test of the $95–$96 volume profile zone per the broader commodities market outlook.

For cross-asset traders, the cleaner near-term expression is long Brent vs WTI spread (North Sea scarcity premium) or long NOK/short GBP as capital allocation signals materialize in currency flows.

Trade WTI Light Crude Oil on CoinUnited.io

Trade WTI with up to 1000xx leverage → | Create Free Account

Frequently Asked Questions

It's a medium-term structural bullish for supply tightness (less UKCS capex = slower future production), but the immediate WTI price effect is modest. The live $6.85 daily range is the dominant risk factor — at 50x leverage, a 2% adverse move wipes out your margin before any structural theme plays out.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.