Quick Links

EnSilica Wins $75M Satellite Chip Contract — Space-Comms ASIC Play Surges 11%

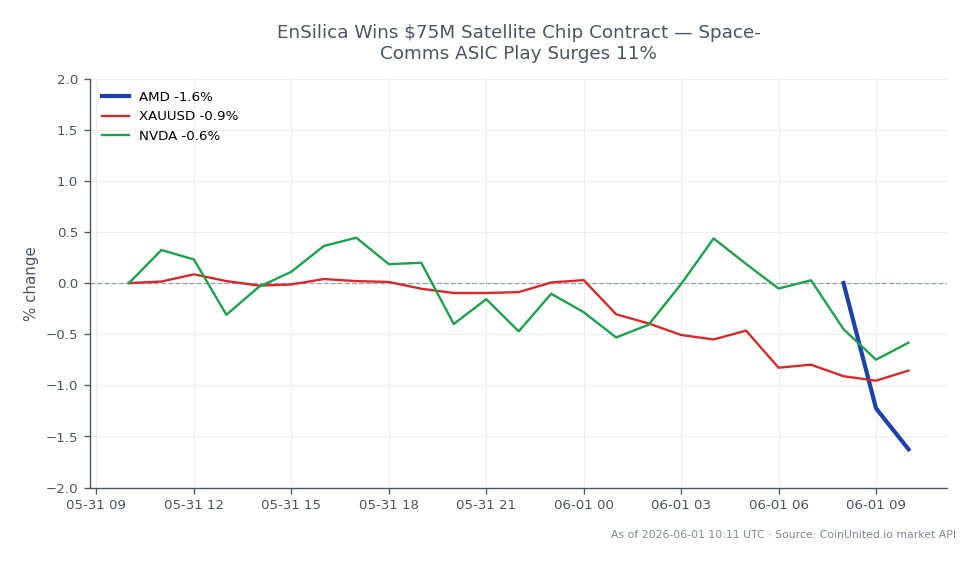

Data Snapshot

Key Takeaways

- •EnSilica secured a contract worth up to ~$75M lifetime value with a leading European satellite operator, covering both payload and user terminal chips across space and ground segments.

- •Shares jumped ~11% on the announcement, confirming material price impact; the deal strengthens a ~£250M lifetime order book and supports the path to cash-flow positivity by late 2026.

- •The contract marks a strategic shift from design services to recurring, high-margin chip supply — the key re-rating trigger the market has been watching.

- •UK Space Agency co-funding of up to $3M signals sovereign backing, adding non-dilutive funding optionality to the programme.

- •Major volume revenues (>$50M) don't begin until 2030, meaning execution risk, programme delays, and potential equity raises remain live risks for traders.

EnSilica plc (AIM: ENSI), a UK-based fabless semiconductor designer, announced a major contract win with a leading European satellite operator covering both satellite payload and user terminal chips —

Event Analysis

EnSilica plc (AIM: ENSI), a UK-based fabless semiconductor designer, announced a major contract win with a leading European satellite operator covering both satellite payload and user terminal chips — a combination of custom ASICs and semi-standard ASSPs. According to Share-Talk, shares jumped approximately 11% on the session, confirming market recognition of this as a material, price-moving catalyst. The disclosed financial structure includes $6.8m in non-recurring engineering (NRE) revenues across FY26–FY28, up to $3m in potential matched funding from the UK Space Agency, and a long-term chip supply opportunity exceeding $50m from 2030 based on user terminals alone — with payload chip revenues still unquantified. On a lifetime basis, the aggregate opportunity reasonably reaches the $75m range cited in market coverage.

What makes this contract structurally significant is not just the headline value but the dual-segment scope. By winning both the space and ground segments of the same satellite programme, EnSilica has entrenched itself as the silicon backbone across the full system stack. This is precisely the strategic corporate partnerships model that drives re-rating in small-cap semis: sticky, long-duration relationships that convert design wins into recurring production revenue. For a fabless company with ~37% YoY revenue growth and chip-supply revenues already up 34%, this contract validates the business model pivot away from pure design services.

The UK Space Agency co-funding element also signals continued sovereign support for domestic semiconductor and space capabilities — a qualitative tailwind within the broader semiconductor supply chain geopolitics narrative. EnSilica's lifetime order book is cited at approximately £250m in independent analyses, and this win adds high-visibility, long-dated volume to that pipeline. It also bolsters the company's path toward EBITDA positivity and cash-flow inflection targeted for late 2026 — the critical valuation hurdle the market has been monitoring. This fits squarely within the mega financing & partnership catalyst theme reshaping small-cap tech valuations.

What This Means for Traders

For single-stock traders, ENSI is the direct play. The immediate 11% price reaction absorbed part of the news premium, but the longer-term investment case centres on whether EnSilica can sustain execution through 2030 when volume chip supply revenues materialise. Positive EBITDA in H1 FY26 combined with a growing order book could catalyse a meaningful multiple re-rating — particularly if subsequent announcements quantify the payload chip revenue, which remains unpriced. The risk side includes execution delays, concentration risk in a single large programme, and potential follow-on equity issuance (the company completed a £10m raise previously to fund growth).

For broader sector positioning, this deal offers a mild positive read-through for European space-comms and niche ASIC design peers, reinforcing the theme that specialised fabless designers can capture major satellite silicon content. The AI monetization & chip demand surge narrative has focused heavily on hyperscale compute, but this contract is a reminder that space infrastructure represents a parallel, growing demand vector for high-reliability custom silicon. Cross-market implications for large-cap names like NVIDIA or AMD are negligible given EnSilica's scale, but the deal reinforces structural semiconductor demand broadly. Since ENSI trades on London's AIM market, CoinUnited's stock CFD coverage means traders can monitor and act on related names without session gaps.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

Frequently Asked Questions

The majority of the contract value ($50M+) only materialises from 2030, so the market is discounting execution and schedule risk. Near-term NRE revenues of $6.8M are meaningful but modest relative to the headline figure.

Continue Exploring

Disclaimer: This brief is for educational purposes only and is not investment advice.