روابط سريعة

Japan 30-Year JGB Yield Hits Record High: Leverage Playbook for JPY, Nikkei & Global Rates

لقطة بيانات

النقاط الرئيسية

- •Japan's 30-year JGB yield reached a record 3.185% (extending to 4.20% in May 2026 per Trading Economics), driven by 3.5% core CPI and fiscal concerns.

- •Leveraged USD/JPY longs at 162.54 face liquidation within ~0.6% on 100x; intervention risk is historically elevated above 160 with no advance warning.

- •Carry trade unwind risk is the key cross-market tail: higher JGB yields compress AUD/JPY and EUR/JPY differentials, threatening cascading volatility.

- •Gold in JPY terms remains structurally supported even as USD-gold faces headwinds from rising real yields.

- •Global bond markets are not immune — Reuters confirmed the JGB move tracked a parallel rise in U.S. Treasuries, signaling coordinated duration repricing.

According to Reuters, Japan's 30-year government bond yield surged to an all-time high of 3.185% amid a sustained week of selling, driven by twin pressures: April core CPI printing at 3.5% year-over-y

Event Summary

According to Reuters, Japan's 30-year government bond yield surged to an all-time high of 3.185% amid a sustained week of selling, driven by twin pressures: April core CPI printing at 3.5% year-over-year — the fastest pace in over two years — and deepening fiscal sustainability concerns. The 40-year JGB yield simultaneously reached 3.675%. Trading Economics data subsequently shows the 30-year yield extending further to 4.20% in May 2026, confirming the scale of this structural repricing.

A weak 20-year bond auction earlier in the sell-off episode underscored declining appetite for long-duration Japanese debt. Only after yields reached historically attractive levels did demand recover, with Reuters reporting a 30-year auction bid-to-cover ratio of 4.55 versus a prior 2.94. The BOJ inflation overshoot policy risk theme is now firmly in play, with markets pricing ongoing pressure on the Bank of Japan to maintain or accelerate its tightening cycle.

Leverage Impact Analysis

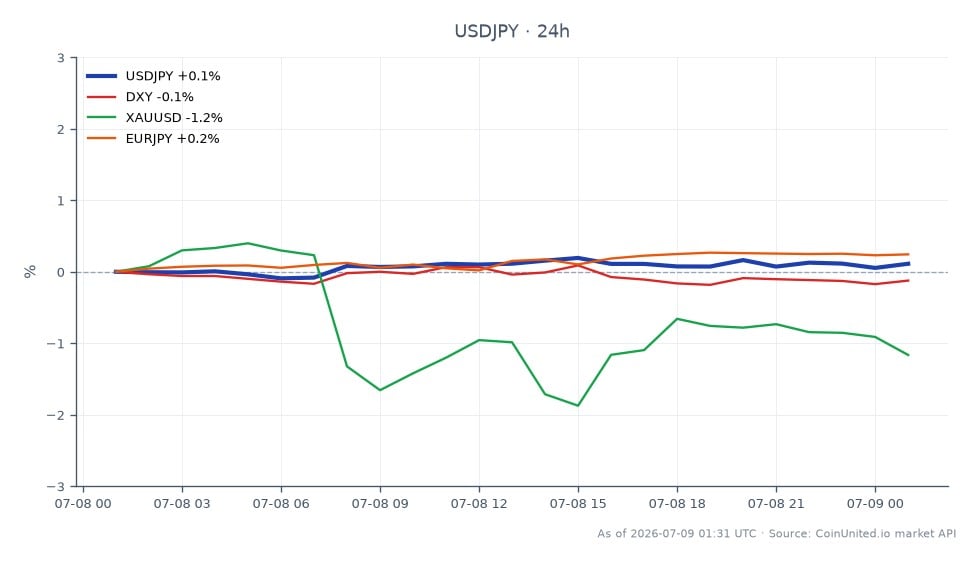

The super-long JGB sell-off creates asymmetric risk for leveraged positions across JPY pairs and Japanese indices. USD/JPY is currently trading at 162.54 (24h range: 162.36–162.61) — multi-decade highs where intervention risk is elevated.

Scenario 1 — JPY Short (USD/JPY long): A 100x long USD/JPY position entered at 162.54 requires only a ~100-pip adverse move (~0.6%) to face full margin wipeout. With BoJ rhetoric increasingly hawkish and yield differentials compressing, any surprise policy signal could produce a 200–300 pip yen strengthening spike. At 50x leverage, margin buffer doubles but a 1.2% move still liquidates the position.

Scenario 2 — Nikkei short via JAP225 CFD: A 50x short JAP225 CFD benefits if rising yields compress equity valuations, but disorderly yield moves historically trigger sharp intraday reversals. Position sizing below 1% of account equity is prudent given elevated bond-market volatility.

Carry trade unwinds are the critical tail risk. Higher Japanese yields reduce the yield differential that funded global carry trades in AUD/JPY and EUR/JPY, and a rapid unwind can produce cascading volatility across emerging markets and risk assets simultaneously. Monitor open interest on JPY pairs for confirmation signals.

Cross-Market Impact

The ECB & BOJ macro inflation divergence is reshaping global duration allocations. As Japanese yields become more competitive, international investors may reallocate away from U.S. Treasuries — Reuters explicitly noted the JGB move followed a parallel rise in U.S. yields, reinforcing the global rates correlation.

Gold: Rising real yields are theoretically a headwind for gold, but fiscal stress and macro uncertainty have kept the inflation hedge bid intact. Gold priced in JPY remains elevated, supporting gold even if USD-gold faces yield pressure.

DXY & Forex: A structurally stronger yen from yield convergence is a DXY headwind. EUR/JPY faces directional risk if ECB-BoJ rate differentials narrow. The macro inflation pressure dynamic detailed in our BOJ Policy & Japan Inflation guide remains the key framework here.

Japanese Equities: Bank and insurer stocks benefit from steeper yield curves on margin improvement, but mark-to-market losses on bond portfolios cap the upside. Growth-heavy Nikkei constituents face discount-rate pressure.

Trading Considerations

For USD/JPY, the 162.00 level is a key near-term support; a break below re-targets 160.80 (recent post-NFP low). Resistance sits at the 162.61 intraday high. The primary risk remains a BoJ emergency statement or intervention signal — historically triggered above 160 with limited warning, as covered in our Japanese yen intervention guide.

Watch the next JGB auction demand metrics and BoJ Governor Ueda's commentary for whether yields are being managed or allowed to reset higher. Fiscal expansion headlines remain a persistent upside driver for JGB yields and a source of APAC stagflation and currency stress.

Trade US Dollar / Japanese Yen on CoinUnited.io

Trade USDJPY with up to 2000xx leverage → | Create Free Account

الأسئلة الشائعة

A 100x long USD/JPY at 162.54 can be liquidated by a ~100-pip yen strengthening move (~0.6%), which is well within the range of a single BoJ policy statement. Reducing leverage to 20–30x or using hard stop-losses above recent highs is critical at these multi-decade extremes.

تابع الاستكشاف

إخلاء المسؤولية: هذا الملخص لأغراض تعليمية فقط وليس نصيحة استثمارية.