روابط سريعة

San Mateo Midstream's $752M Cardinal Acquisition: Delaware Basin Consolidation Accelerates

لقطة بيانات

النقاط الرئيسية

- •San Mateo Midstream JV (Matador 51%, Five Point 49%) is reportedly acquiring Cardinal Midstream for ~$752M, its largest external deal to date — though formal SEC/press release confirmation is still pending.

- •The deal adds gathering and processing capacity to San Mateo's existing 900+ mile Delaware Basin network, supporting third-party revenue diversification and a higher JV valuation.

- •MTDR equity is the primary tradeable lever; a JV-level debt funding structure is bullish for Matador's corporate balance sheet, while equity injection scenarios would raise leverage concerns.

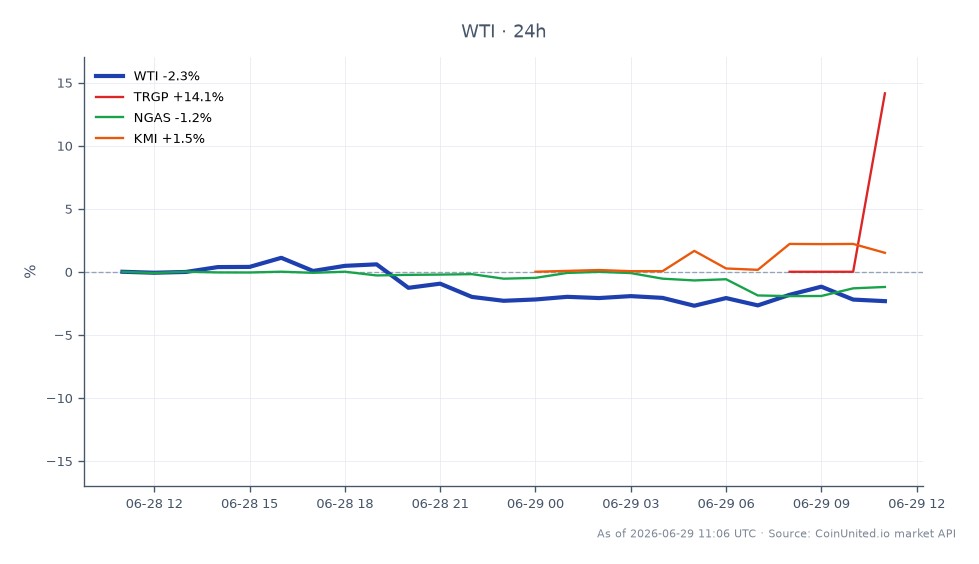

- •Midstream peers ONEOK, Kinder Morgan, and Targa Resources may see updated comp multiples as analysts benchmark this private-asset transaction price.

- •Near-term WTI and natural gas price impact is minimal, but expanded Delaware Basin processing capacity is a structural medium-term supply positive.

Matador Resources Company's (NYSE: MTDR) midstream joint venture, San Mateo Midstream LLC, is reportedly acquiring Cardinal Midstream for approximately $752 million, marking one of the larger private

Event Analysis

Matador Resources Company's (NYSE: MTDR) midstream joint venture, San Mateo Midstream LLC, is reportedly acquiring Cardinal Midstream for approximately $752 million, marking one of the larger private midstream transactions in the Delaware Basin's recent M&A cycle. San Mateo is co-owned by Matador (51%) and private infrastructure investor Five Point Energy (49%), giving both sponsors significant skin in the deal. According to Matador's public disclosures, San Mateo already controls over 900 miles of pipelines and 19 saltwater disposal facilities, with its Black River Cryogenic Processing Plant slated for capacity expansion from 60 MMcf/d to up to 260 MMcf/d — making Cardinal's gathering and processing assets a logical bolt-on.

This deal is consistent with San Mateo's established acquisition playbook. Prior transactions — including Matador contributing its Pronto Midstream subsidiary at an implied ~$600 million valuation for $220 million upfront cash — show the JV scaling systematically toward a fully integrated Delaware Basin midstream platform. The Cardinal acquisition, if confirmed at $752 million, would represent the JV's largest single external purchase to date and signals confidence in long-term Delaware Basin throughput growth. Note: as of publication, this transaction has not yet appeared in primary SEC filings or formal Matador press releases and should be treated as market-reported.

Strategically, the deal reduces Matador's midstream bottleneck risk and diversifies San Mateo's third-party customer base — a key valuation driver for midstream platforms. More third-party volumes means less revenue concentration tied to Matador's own drilling cadence, which is exactly what analysts want to see ahead of any potential future San Mateo monetization (IPO, additional JV sale, or dropdown). This fits squarely within the broader global acquisition and consolidation wave sweeping U.S. energy infrastructure.

For the midstream sector broadly, the transaction provides a fresh private-asset valuation data point. Peers such as ONEOK, Inc., Kinder Morgan, Inc., and Targa Resources, Inc. are direct comparables in the gathering and processing space, and analyst comp tables will likely be updated once deal terms are formally disclosed.

What This Means for Traders

The primary listed exposure is MTDR equity. If the acquisition is confirmed with a credible funding mix — JV-level debt secured against midstream assets rather than Matador's corporate revolver — the market is likely to treat this as a positive sum-of-the-parts story. San Mateo's expanded scale and third-party revenue mix should support a higher implied valuation for Matador's 51% stake. However, if investors perceive Matador is injecting significant equity capital or guaranteeing JV debt, leverage concerns could weigh on the stock near-term. Matador previously targeted ~1.1x leverage after using Pronto midstream proceeds to pay down its revolver — traders should watch for any updated balance sheet guidance.

For the energy sector acquisitions thematic, this deal reinforces the M&A acquisition wave narrative in U.S. midstream. Midstream comparables — particularly Permian/Delaware-focused names — may see modest sympathy moves as analysts refresh EV/EBITDA comp tables. Natural gas and WTI crude traders should note that expanded gathering and processing capacity structurally supports higher regional throughput, a mild long-term supply-side positive, though the near-term price impact on benchmarks remains limited.

Sentiment overall is cautiously constructive for MTDR and the midstream peer group, but confirmation of deal terms and financing structure is the critical catalyst before taking a strong directional view. This is a story requiring formal disclosure before meaningful repricing occurs.

Start Trading on CoinUnited.io

Create Your Free Account → — Trade crypto, stocks, forex, indices, and commodities with up to 2000x leverage and zero fees.

الأسئلة الشائعة

As of publication, the deal has not appeared in Matador's SEC filings or formal press releases and is treated as market-reported. Traders should await official confirmation before sizing positions.

تابع الاستكشاف

إخلاء المسؤولية: هذا الملخص لأغراض تعليمية فقط وليس نصيحة استثمارية.